Yields on the 10-year Treasury, after a brief dip at the start of the week, returned to the upper 4.2% range, even briefly breaking 4.3%, in reaction to inflationary pressures from the Iran conflict.

In turn, this led mortgage rates to increase by 11 basis points

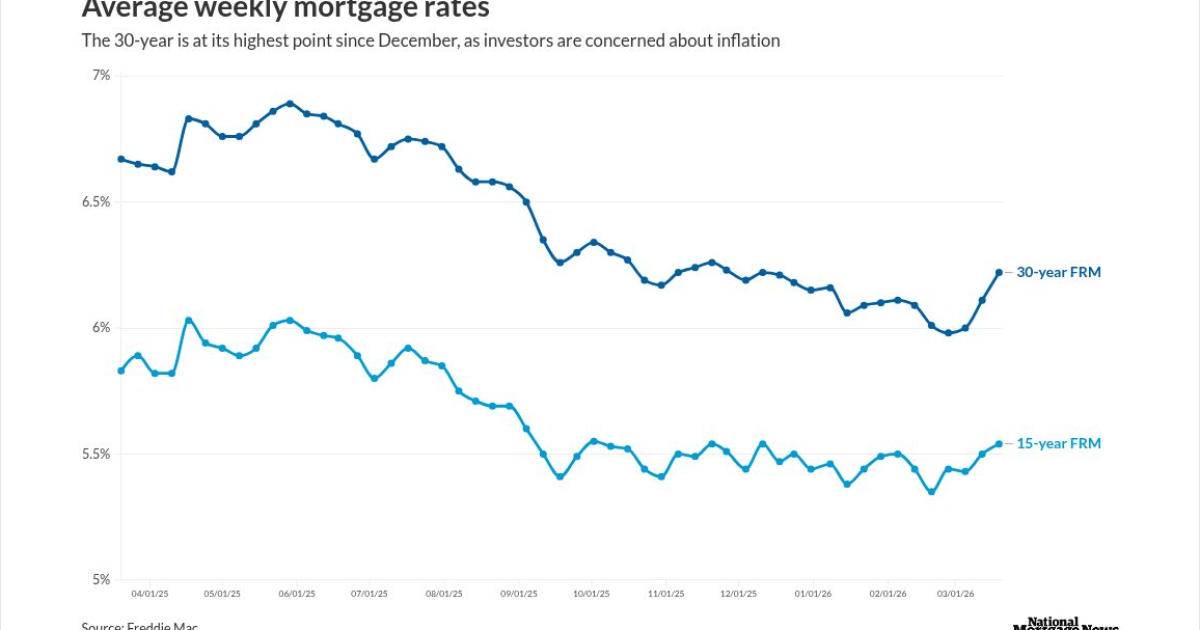

The 30-year fixed rate mortgage averaged 6.22% for March 16, up from 6.11% a week ago and 6% on March 5; this rate was at 5.98% on Feb. 26. For

This is the highest the 30-year has been at since the start of December.

However, the 15-year FRM had a smaller gain, just 4 basis points to 5.54%. This compares with 5.83% from a year ago.

How mortgage rates compare versus last year

The 30-year is still about a half-percentage point lower from last year, Sam Khater, Freddie Mac's chief economist, pointed out in a press release.

"Potential homebuyers are poised for a more affordable spring homebuying season than last with the market experiencing improvements in purchase applications and pending home sales," Khater added.

The Federal Open Market Committee's

"Mortgage rates moved decisively higher this week as the war in Iran continues to stoke inflation fears," said Kate Wood, NerdWallet's home and mortgage expert, in a Thursday morning comment.

Wood pointed out investors aren't using bonds as a safe harbor because they have concerns inflation will erode their value.

How bond investors are reacting

"Lower prices mean higher yields, and mortgage rates have been heading up with those higher yields," Wood said.

As of 11 a.m. on Thursday, the 10-year yield was at 4.27%, flat versus Wednesday's close, along with March 13.

The conforming 30-year FRM as tracked by Optimal Blue was at 6.215% as of Wednesday, its highest point since mid-October.

If the Iran conflict is short-lived, then mortgage rates are likely to move lower again, Lisa Sturtevant, chief economist at Bright MLS said in a statement following the FOMC meeting.

Derailing the spring homebuying season at a minimum

"However, if the conflict is prolonged or expands, the result could be higher inflation and higher mortgage rates," Sturtevant said. "In that case, we may be looking not just at a delay in the spring homebuying season, but at a broader shift in the trajectory of a housing market that had been expected to rebound in 2026."

Eric Orenstein, senior director at Fitch Ratings, was similarly pessimistic.

"Rate uncertainty has chilled some of the exuberance about mortgage volumes for the year," Orenstein in his post-FOMC comments. "We may still see the 30-year dip back below 6%, but a refinance rally feels farther away than it did a month ago."

The Mortgage Bankers Association's Weekly Application Survey reported

"Whether this upward pressure on rates — tied to Middle East tensions — will temper what should be strong spring demand remains to be seen," Bob Broeksmit, MBA's president and CEO, said in a Thursday morning statement. "Purchase activity, however, continues to hold up, supported by improving housing inventory."

Are buyers in the driver's seat?

Buyers are not deterred by rates around 6%, said Barb Cooper, a Redfin agent from Austin, Texas.

"Buyers are in the driver's seat, and they can negotiate by offering less than the asking price and/or asking for seller concessions to lower their monthly payment," Cooper said in a press release. "The upside of higher rates is that they decrease competition, so buyers can try to get everything they want."

While rates are not keeping buyers away, the rising costs related to homeowners insurance and property taxes are sidelining some people, Cooper added.