- Key Insight: Cash loans made by the Federal Home Loan Banks dipped in the third quarter versus a year ago.

- What's at Stake: Experts looking for insight into the economy cautioned against interpreting the dip as a sign of abundant liquidity.

- Expert Quote: "I don't think this is a sign that the financial system is awash in liquidity." — Kathryn Judge, Columbia Law School

Market uncertainty and a dearth of financial data spurred by the recently concluded government shutdown has led to renewed interest in data from the Federal Home Loan Banks to gain insight into the strength of the banking system.

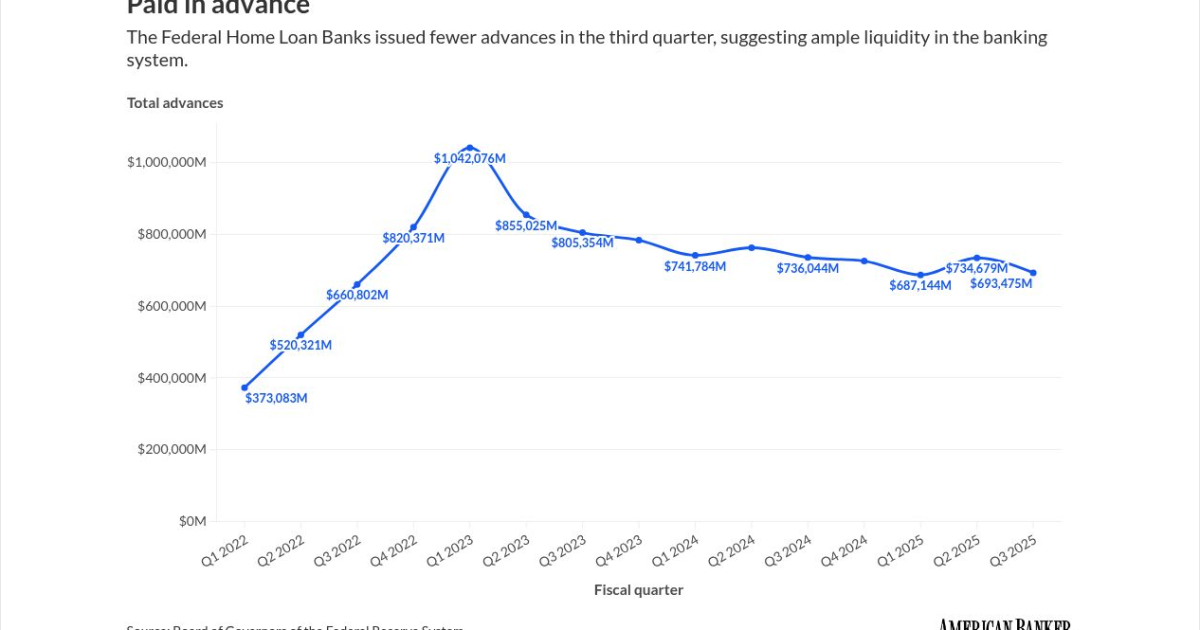

Cash loans to commercial banks and other members dipped 6% in the third quarter to $693.5 billion, from $736.7 billion a year earlier, the Federal Home Loan Banks said in an

Lower advances generally mean that money is cheaper elsewhere or that banks are flush with cash — or both.

But Kathryn Judge, the Harvey J. Goldschmid Professor of Law at Columbia Law School, cautioned against reading too much into the FHLBs' earnings and the volume of advances, which she said can vary "quite significantly" over time.

"I don't think this is a sign that the financial system is awash in liquidity," said Judge.

She noted that the Federal Reserve has said it will

"The Fed's decision to end QT, for example, suggests that liquidity is becoming more scarce than it has been in quite a while," Judge said.

The dip in FHLB advances comes amid a dearth of financial data due to the government shutdown. The Bureau of Labor Statistics has not been able to collect hard data in September and October, which has caused significant delays in the official jobs reports, at a time when the Trump administration is

Ryan Donovan, president and CEO of the Council of Federal Home Loan Banks, the FHLBs' trade group, said advances expand or contract based on banks' needs.

"The Federal Home Loan Banks were established to be a reliable source of affordable liquidity for their members when they need it," Ryan said. "This is the fundamental nature of the FHLBank System, and quarter over quarter, year over year, the FHLBanks have demonstrated their dependability, providing their members with liquidity that anchors communities nationwide."

FHLB borrowing has been a topic of interest since the

Before that, when the pandemic hit in March 2020, member institutions tapped the FHLBs in droves, with advances spiking to $807 billion. But when federal stimulus programs kicked in, financial institutions were themselves flooded with deposits and advances tanked.

The 11 FHLBs are member-owned cooperatives, but have been chartered by Congress to provide liquidity to the financial system as a means of supporting home development. The FLB system issues debt with an implied guarantee, making the FHLBs a lesser-known Government-Sponsored Enterprise than its cousins, Fannie Mae and Freddie Mac.

That dual mission of providing liquidity and supporting housing came under intense scrutiny during the Biden administration, when the former FHFA Director Sandra Thompson proposed important changes to the system following a

The Council of Federal Home Loan Banks maintains that the system's primary mission is providing liquidity to members, while 10% of FHLB profits go to affordable housing and community development programs. Last year, the FHLBs contributed a record $1.2 billion to affordable housing and community development.

Some critics of the system have claimed the federal government subsidizes the FHLBs, which also pay large dividends to members, through its implied guarantee.

Last week, the

Last year, a study by the