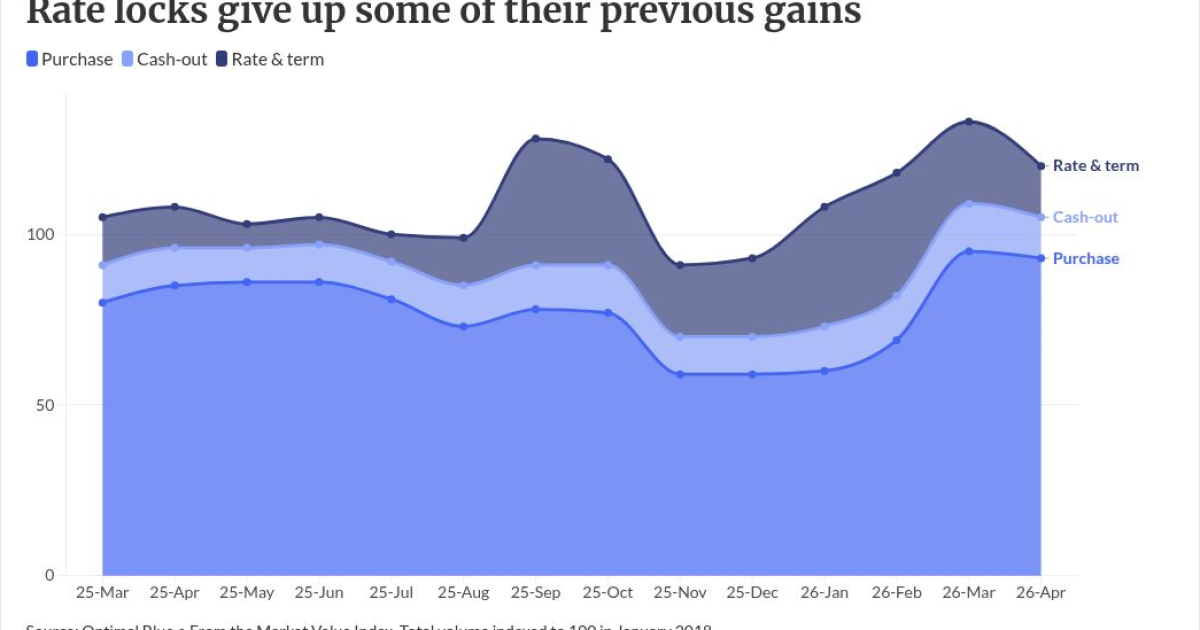

Rate locks on home loans fell in April with a particularly steep dive in refinancing activity as the impact from March's higher financing costs reversed some previous gains.

Overall, locks fell 9% from

The declines could prove fleeting given

"April looks more like a cooling from a strong first quarter than a real weakening in borrower demand," said Mike Vough, senior vice president of corporate strategy at Optimal Blue, in a press release.

Year-ago comparisons

Even with declines relative to March, generally April's lock numbers were higher than they were a year earlier.

Optimal Blue, which indexes total volume to 100 in October 2018, recorded a level of 121 last month, up 11% from 12 months ago. Purchase loan locks rose 9%, rate-and-term refinancing jumped 22% and cashouts were 11% higher than a year earlier.

Refinancing accounted for nearly one-fourth or 23% of all locks, down from April's level of 28% but in line with where refinancing share was during much of last year.

The purchase pull-through rate was higher on the month but down compared to a year ago at more than 82%. Refinances had a pull through rate just shy of 79% that was up notably compared to the previous month and a year earlier.

Product mix developments

The

The Federal Housing Administration-insured loan share was 19%, and the percentage of mortgages that the Department of Veterans Affairs guarantees clocked in at 13%. Adjustable-rate mortgages represented 10% of locks.

The nonconforming share was 17% with loans made outside the qualified mortgage definition at 9%. Non-QM guideline expansion occurred primarily in bank-statement and investor loans.

Secondary marketing and servicing

Indicators of credit quality and the ability to repay were largely stable in April, including the first-time homebuyer share, debt-to-income ratios and scores.

Higher rates and lower refinancing gave a boost to the valuations for mortgage servicing rights. MSR values increased 5 basis points to 1.29%, with the acquisition price was 5.16 times the annual servicing fee income, according to Optimal Blue.

Agency mortgage-backed securities execution picked up momentum while bulk activity declined. The investor count picked up slightly for the first time in awhile.

"The move toward agency MBS execution, combined with higher MSR values and increased investor participation continues to prove that lenders need to evaluate all potential execution options to maximize profitability," Vough said.