Better Home & Finance remains squarely in the red, but executives remain adamant the company will hit a long-promised benchmark this year.

The lender recorded quarterly and annual growth in revenue and originations but still posted a $70 million net loss for the first quarter, it said Thursday. That mark includes a $20.9 million net loss from discontinued operations

Even putting aside that $20.9 million, Better's net loss was still significant following

Company leaders Thursday reaffirmed their long-stated goal to reach breakeven adjusted EBITDA by the end of this third quarter, and Better shaved its adjusted EBITDA loss to $19 million in the recent period. Founder and CEO Vishal Garg said the EBITDA goal would stand, even if macroeconomic factors don't improve.

"We're going to have to cut costs deeper," he said in response to an analyst's question about the goal. "I think we're pretty committed to that number."

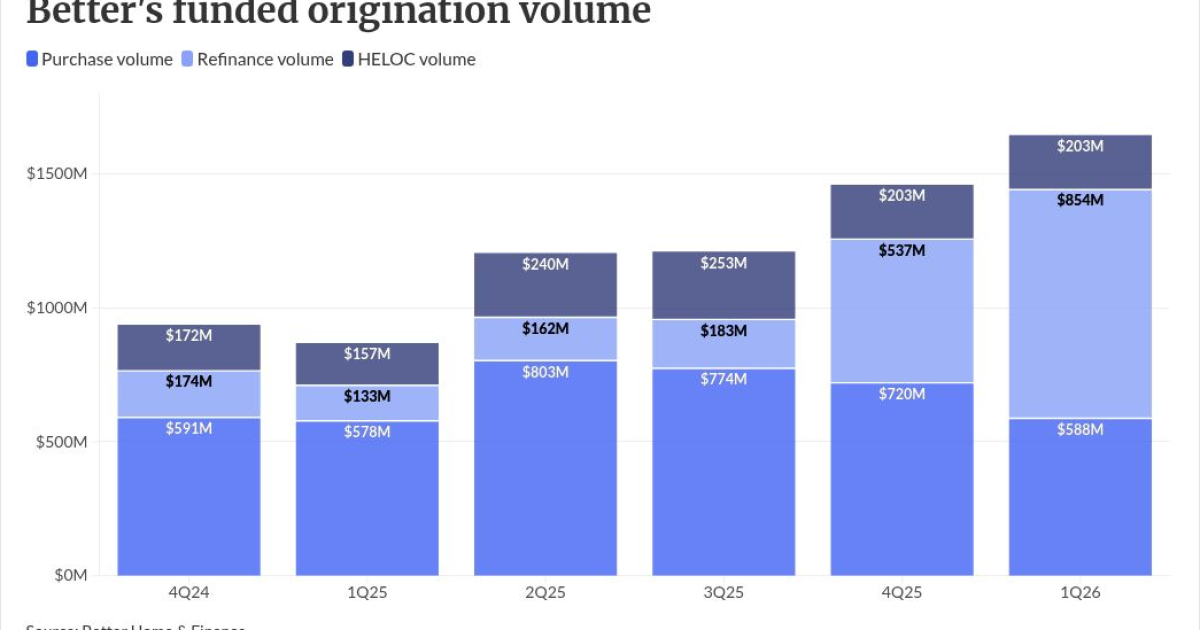

The lender reported total loan volume of $1.64 billion in the first quarter, up 12% quarterly and 89% annually. Production blossomed with $854 million in refinance volume, and $203 million in home equity line of credit volume, a slight quarterly increase.

Demand wavers

Garg said the company's goal of $1 billion in originations a month would be deferred, as the Iran conflict has rattled the economy and

"We think that's a coil spring for when things die down in the Middle East," he said. "You're going to see some bumper months as we convert all those customers who are effectively on a wait list to lock when rates come back down."

Better said those higher-margin HELOCs are factored into a slightly higher second quarter earnings guidance for loan volume and revenue, which assumes no improvement in macroeconomic conditions.

The company posted revenue of $48 million in the first quarter, up slightly from the end of 2025. The third quarter breakeven adjusted EBITDA target will require revenue around the low-to-mid $70 million range, said Chief Financial Officer Loveen Advani.

Green shoots

The lender this month announced $25 million in annualized cost reductions, including its pending divestiture of the UK bank. Better's warehouse capacity also expanded from $575 million at the end of the fourth quarter to $850 million in the first quarter. It retains cash and cash equivalents of $136 million.

Garg said the macroeconomic backdrop has been a boon for

"We're starting to see a lot more inbound from other fintechs, other large consumer credit companies, to pivot from their traditional unsecured offerings into a secured offering like a HELOC," he said.

Better's stock opened at $34.16 per share Thursday morning, but fell to $30.98 per share by mid-morning following the earnings call.