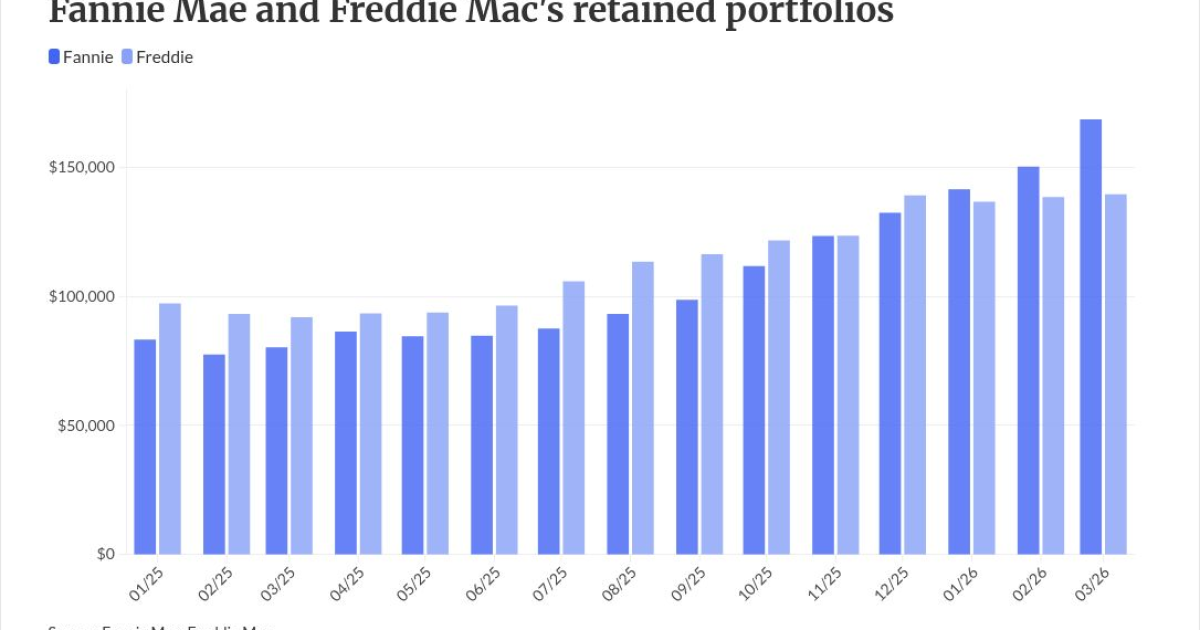

Fannie Mae has reported a jump in its retained portfolio size that investment professionals at Rithm have recently noted is the largest seen since the Great Financial Crisis.

The government-sponsored enterprise retained a combination of loans and mortgage-backed securities totaling nearly $168.74 billion in March, up considerably from the previous month's $150.39 billion. Freddie Mac, in contrast, only reported a rise to $139.76 billion from $138.57 billion.

"Fannie Mae increased its retained portfolio by approximately $18.3 billion in March, the largest monthly addition since 2009," Satish Mansukhani, a managing director at Rithm, and Alan Wynne, a vice president, wrote in a recent report.

The $308.5 billion in both retained portfolios combined that month also marked a high not seen since early 2021, they added.

Given that Freddie Mac was more aggressive than its counterpart for much of the past year, the March activity establishes that there's a different trend at play in 2026.

"These reports showed considerable differences in the pace of

McBride is known for being among the first wave of pundits to foresee the housing bubble that forced the GSEs into government conservatorship in 2008, and Lawler was a senior vice president at Fannie in the pre-crisis era.

The blog indicates that the driver of the disparity between the two GSEs' retained portfolios is unclear, but suggested it could be related to growing market-value sensitivity of the retained portfolios to rate swings.

Models suggest that as of the end of March, Freddie would take more losses in response to a theoretical 50 basis-point jump in rates than Fannie, according to the blog.

Retained portfolios and "IPO" prospects

Some analysts like those at Keefe, Bruyette & Woods have viewed retained portfolio expansion as being conducive to a plan to stage the first new offering of GSE stock in some time because it is

Combined with the expansion of the investments portfolio, growth in the retained one was the main driver of net interest-income growth fueling

Retained portfolio growth may help build capital that could support interest in an "initial public offering" of enterprise shares, but it

Fannie's net worth would already exceed standards if the enterprises were to reduce their current requirements to 2.5% of risk weighted assets, according to a recent Mizuho report. Freddie could meet that standard after a year of earnings retention.

However,

Both Wedbush and Mizuho have forecast that rebuilding capital could take several years under current standards.

Mizuho recently put 30% odds on a "fast exit" from conservatorship with lower capital standards that could accommodate a secondary stock offering for Fannie. It put 20% odds on the same happening at Freddie.

Trump administration officials have shown interest in a new offering for