As the feedback period for the latest Basel proposal nears, some experts predict a key concern for nondepository home mortgage lenders will be the increased credit conversion factor for warehouse line commitments that aren't unconditionally cancelable and mature within a year.

Proposed changes that may in some cases raise the CCF to 40% for unused, short-term

"The expanded commitment definition, and the potential impacts, would be extremely punitive," he said.

That is significant because nondepositories dominate home mortgage lending and need lines that have unused capacity to manage things like fluctuating volumes and meet liquidity standards that government-related agencies have.

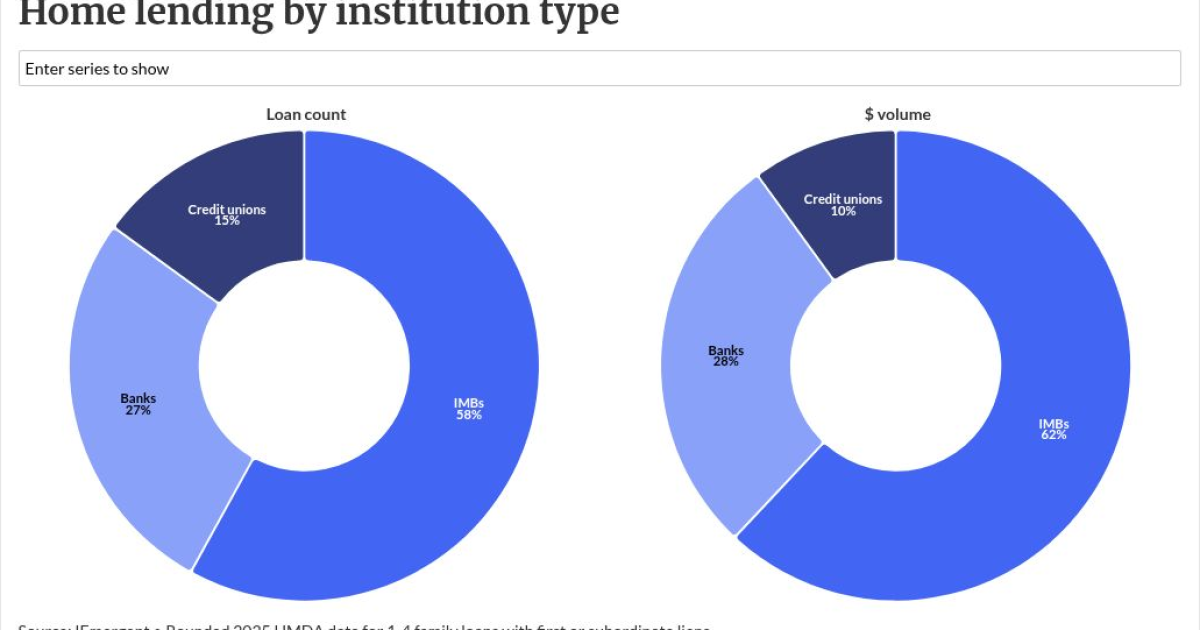

Independent mortgage bankers reliant on warehouse financing accounted for nearly 58% of originations by count and nearly 62% based on dollar volume in 2025, according to iEmergent's analysis of available Home Mortgage Disclosure Act data.

"Warehouse lending is a very important part of the mortgage ecosystem," Oswald said.

Overall, the Mortgage Bankers Association found that while the current Basel plan has improved relative to past versions, "certain aspects continue to overstate the risks associated with key mortgage-related assets and activities."

Oswald acknowledges some other proposed Basel changes lower risk weights on warehouse lines more broadly, particularly for large banks. In isolation, that development may encourage competition, potentially lowering nondepository line costs in the short term. But it also could lead to consolidation.

"That part of the proposal could, in isolation, mean more entrants into the space. You'd see much more competitive pricing. Effectively, you could see a race to the bottom because margins are so thin, and people want to capture market share," he said.

When asked about the net impact of the warehouse line changes, Oswald said that the combined impact of the CCF and the expanded definition of commitment swings them too far in terms of taking a conservative view of how much capital to reserve for the risks banks take in this area.

"If the final proposal moves forward as it exists, it could negatively impact housing finance infrastructure in the United States," he said.

The MBA is recommending a change to "provisions that would increase capital requirements on unused portions of warehouse facilities and align capital treatment of funded funded warehouse lines with the risk profile of the underlying mortgage collateral."

Other lending and servicing implications

Oswald acknowledged that some of the Basel proposal's other provisions loosen mortgage-related capital rules in ways that could

Removing the Tier 1 dollar-for-dollar reduction requirement on mortgage servicing assets over 10% (or 25% for large banks) would give bank lenders a more favorable cost of capital and the ability to possibly price more competitively when holding MSRs on loans they want to refinance.

When asked about assertions that this could potentially prompt

"As a bank, you will get a lower cost of capital than you have as an IMB. You will no longer need a warehouse line of credit. You will be able to borrow at a lower rate," he said.

Nonbanks eyeing prospects for converting would also have to consider the expenses associated with operating in a different regulatory environment, he said.

"Once you're a bank, you're subject to a lot more regulation in general including the broader risk and control frameworks under Basel, all of which can be a bit of a maze. There is just a lot there that you would have to comply with that will affect the broader cost comparison," said Oswald.

The Basel proposal's final form will determine how much it will incentivize bank involvement in mortgages or nondepository conversions with the potential for greater benefits if a directive to reexamine and possibly lower the risk weighting for MSRs turns out to be significant.

"If that 250% risk weight isn't significantly lowered, then the impact in terms of banks jumping back into mortgage servicing becomes questionable. The requirement to remove excess MSR from the core capital calculation doesn't really move the needle enough," Oswald said.

MBA has recommended a reduction to 100% based on its analysis of how mortgage servicing assets have historically performed.

Other commenters like the Community Home Lenders of America also have questioned how much impact the proposed Basel changes will have.

"CHLA is skeptical that these risk weight reductions will have any significant impact in bringing banks back into the business of originating mortgage loans," the group wrote in a letter sent to regulators on Wednesday.

"We believe that there are many other business and financial factors that play a more significant role in the banks' broad retreat from the mortgage business," the association added.

The community lenders group expressed support for reductions in MSR and warehouse line risk weightings. CHLA added that it "does not oppose" risk weight reductions for whole loans that are part of the proposal.

Other recommendations the MBA made included lowering the proposed risk weighting for government-sponsored enterprise securitizations, providing recognition for private mortgage insurance, and adjusting rules floated for commercial assets aimed at ensuring "secured real estate lending is not treated more harshly than unsecured corporate exposures."