Improved affordability and increased inventory helped the spring homebuying season get off to a strong start, but the recent rise in mortgage rates has pushed some buyers out of the market, according to ICE Mortgage Technology's latest

"Mortgage rates bottomed near 5.95% early this year, pushing affordability to its best levels in four years and helping drive two of the firmest monthly home price gains we've seen in over a year," said Andy Walden, head of mortgage and housing market research at ICE, in a press release Monday.

"Since then, 30‑year rates have risen roughly 40 basis points, pulling about 4% of buying power back out of the market and reshaping conditions from those early‑year peaks," Walden said. "Even so, 99 out of 100 major markets still saw improved affordability from a year ago, and inventory continues to rebuild. That combination is helping this spring market feel better supplied and more balanced than in recent years, even as rate volatility reasserts itself."

At a 30-year conforming rate of 6.35%, which ICE recorded on March 25, the monthly principal and interest payment needed to buy the average-priced home was $2,169, up $88, or 4%, from February but still down nearly $60, or 3%, from a year ago, the report showed.

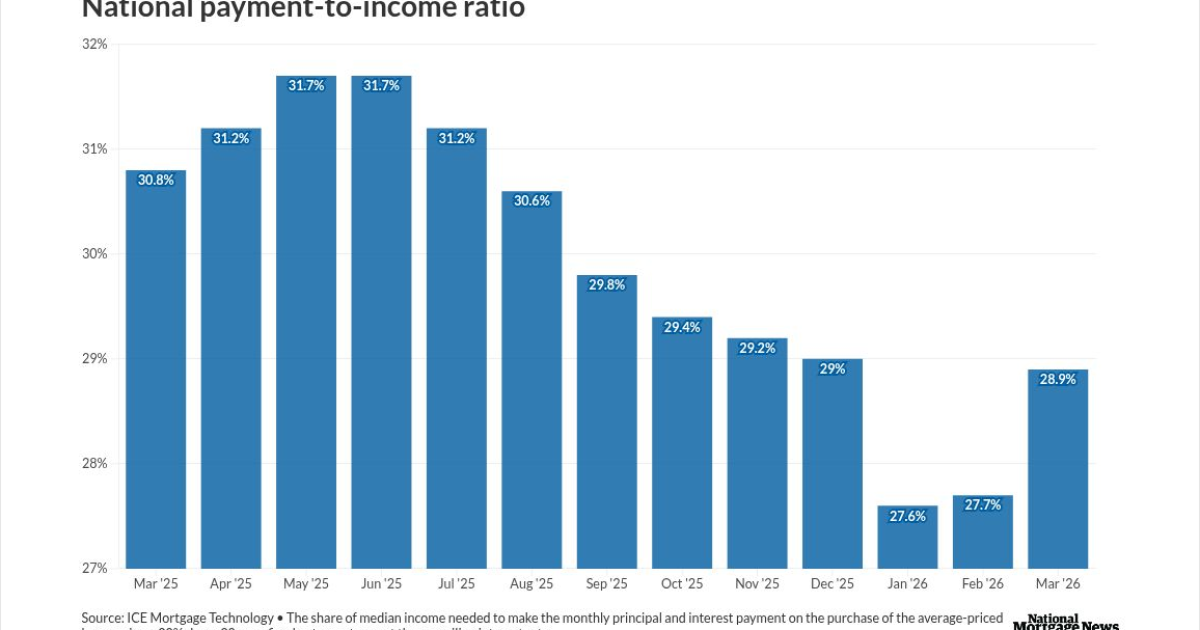

The monthly payment on the median home also equaled 28.9% of the average household income, which was an increase from 27.7% in February and a decline from 30.8% last March.

While housing inventory continues to improve, the pace has been slowing. Inventory climbed 8% year over year in March, the same as February, yet active listings were still 11% below prepandemic levels. The Mountain West and South saw the largest inventory hikes, as about 40% of markets were at or above prepandemic supply, but deep deficits remain across the Northeast, the report said.

The strongest inventory gains over the past six months came in Seattle, Colorado Springs, Colorado, Spokane, Washington, and Denver, each experiencing increases of at least nine percentage points.

Meanwhile, active listings in Hartford and Bridgeport, Connecticut, were still 78% below prepandemic norms, and those deficits have deepened over the last six months, the report found.

Higher rates have also slashed the number of borrowers considered "in the money" for a refinance by about 60% from recent highs. The

"Housing market conditions this spring point to a market that is gradually normalizing, but not evenly," said Bob Hart, president of ICE Mortgage Technology, in the release. "Inventory is improving and affordability remains better than it was a year ago, but conditions still vary widely by geography, price point and borrower profile."