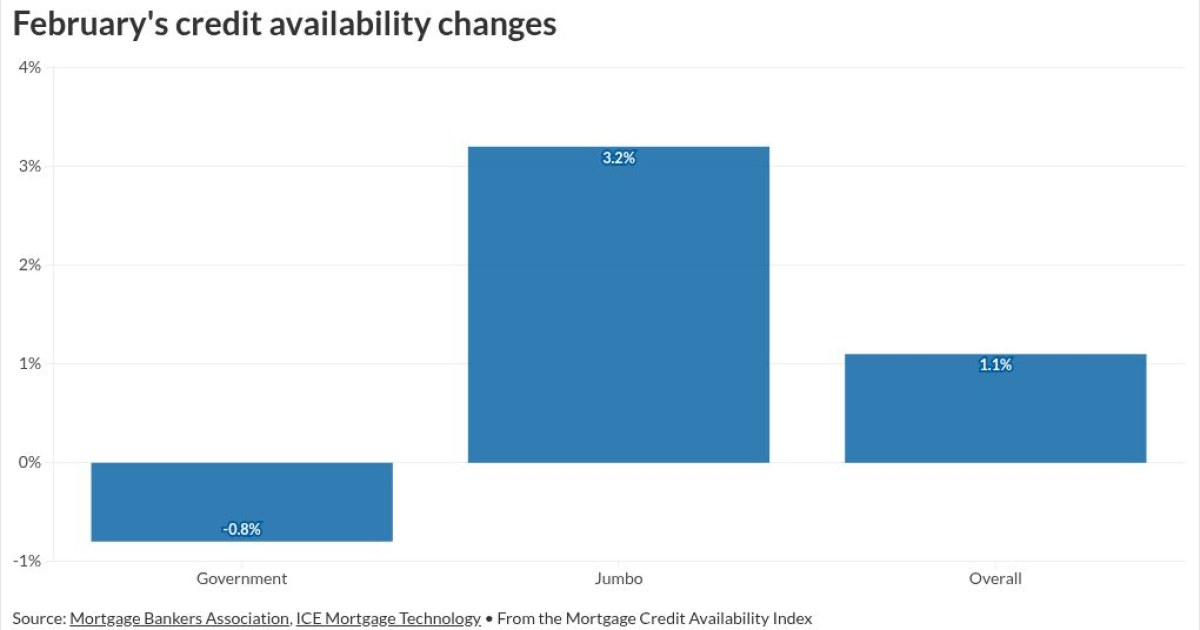

Government loan performance issues prompted tighter underwriting in the past month but credit availability expanded in other parts of the market, according to a Mortgage Bankers Association analysis.

Availability in the jumbo sector, which includes

The two categories represent opposite ends of the spectrum that have become particularly important to watch on the index, which is based on an analysis of ICE Mortgage Technology's data and registered a collective increase of 1.1% to 107.1 for all loan products.

That overall reading is still close to the baseline 100 level that represents 2012's low, suggesting credit is historically tight on a net basis with room to move higher. But the jumbo market's reading is trending upward more markedly than other sectors.

"The jumbo index increased by 3% for the second straight month, again driven by growth in non-QM loan programs," said Joel Kan, MBA's vice president and chief economist, in a press release.

Higher

Underwriting factors to watch

Kan's reference to a focus on LTV limits ratios is in line with recent comments made by Marina Walsh, vice president of industry analysis, which indicate the industry is counting on home prices to buffer loan performance.

"We have this tremendous build up in home equity, and that will help us weather any type of storm, whether that's an economic downturn, whether it's increases in property taxes and insurance, it will help," Walsh told attendees at

"Certainly we have affordability issues, but particularly for those borrowers who originated a loan during the pandemic, or before this home equity accumulation, it will certainly help temper ramifications of any type of economic downturn," she added.

Lenders in the non-QM sector have been expanding some underwriting parameters but they are also setting limits on credit scores stricter than the FHFA and

"FHA mortgages are going to be much more biased towards higher LTV and lower credit," said Jack Kahan, senior managing director and head of the asset- and residential mortgage-backed securities groups at KBRA."The credit scores in the non-QM space just remain like prime."

However, panelists at an MBA servicing panel indicated non QM delinquencies can vary broadly.

Trends in the conforming market

The government-sponsored enterprises' conforming market, which is part of the conventional sector that has a relatively lower MBA delinquency rate of 2.62%, has had more cautious underwriting than jumbo but its credit availability did expand 2% in the past month.

The Trump administration has expressed an interest in having the GSEs not compete with FHA or crowd out the private capital, but its officials have also sought to balance that with an aim to support homebuyer affordability and bring in the type of business that could help them leave conservatorship.

The result has been a general plateau in credit availability with some fluctuation within a narrow range by month.