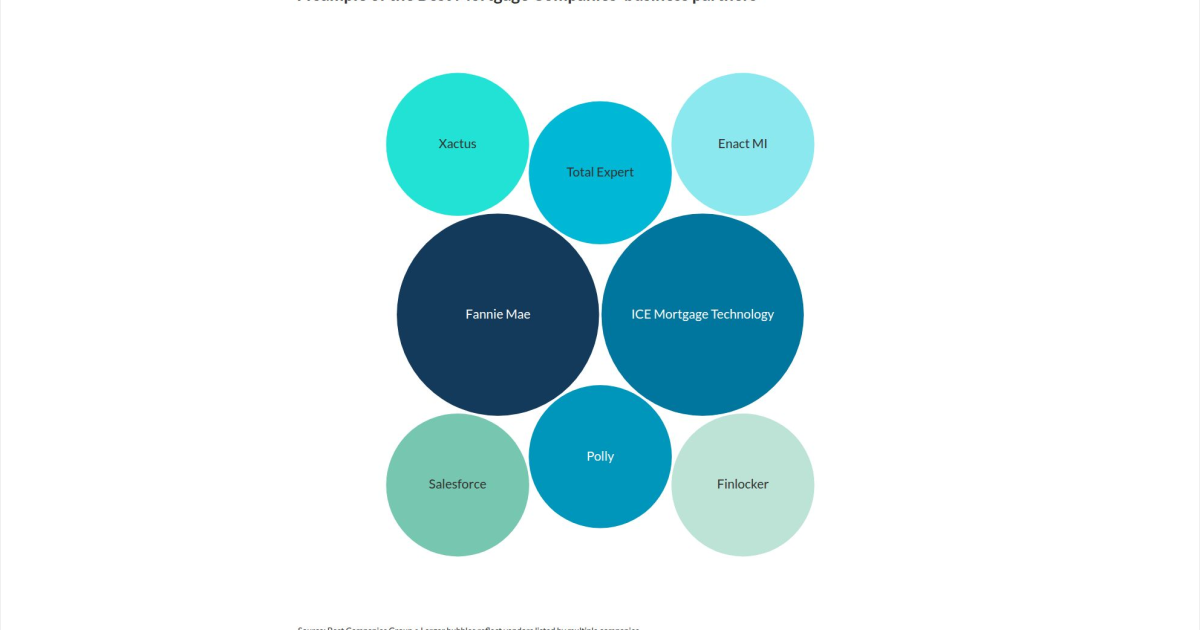

An analysis of some of the vendors that companies in the

Core service and secondary market providers may offer necessary products that accommodate business across the industry, but some of the top employers also distinguish themselves through either more unique integrations or proprietary technology.

Lenders have to ask themselves, "How are you going to differentiate yourself in a world of sameness?" Bill Dallas, chairman of industry consultancy Dallas Capital, said.

That's in line with what some of the Best Companies had to say.

How some of the Best Companies differentiate

Spring EQ said it "embraces cutting-edge technology and welcomes fresh ideas from all team members to drive innovation."

Sales-related tools used to handle customer relationship management and specialized products outside the qualified mortgage definition play central roles in NewFi's employee outreach.

"For us, technology is a key component of recruiting account executives through our custom-configured CRM and broker portal designed for non-QM," a NewFi spokesperson said in a statement.

NewFi also noted in materials supporting its Best Companies application that it offers a bank-statement analysis tool and automation that handles loan estimates and other disclosures for its brokers.

Cardinal Financial has a proprietary loan engine called Octane that supports a variety of products and aims to automate around 90% of the mortgage process for brokers, including changes of circumstance, document management and loan progress tracking.

A focus on cohesive strategies

Whatever vendor and technology mix a company chooses, the key to making them attractive to employees is getting them collectively in a manner that supports loan sales in competitive ways, and with operational expertise, Dallas said.

"The real trick is, how do you glue it all together in something that's coherent to the client? You've got to win at the point of sale," he said.

Atlantic Bay Mortgage Group said in its application materials that its stated goal is to offer "tools and resources for success, including support for high loan volumes."

Estelle Norvell, CEO of Mattamy Home Funding, said she has found that vendor selection "matters more to the front end employee that's out there making the sale and talking to customers."

Keeping an eye on the bottom line

Norvell added that her company's management team gives a lot of thought to which vendors it works with, based not only on how they interact and compare on pricing.

"We're constantly looking at new ones," she said.

Norvell added that decisions around whether to change vendors or how many business relationships will be maintained are managed with an eye on how all of this impacts loan costs.

While working with numerous vendors can get complicated, Norvell said her company weighs this against the ability to comparison shop among business partners such as mortgage insurers.

"They may have lower rates for whatever reason on certain products or or certain parameters at different times," she said. "We work to give the buyer the best possible deal we can, so we may not tie ourselves to one vendor."