UWM Holdings again said it is "prepared to consider enhancements" to its offer for Two Harbors if its board was willing to engage.

In its latest letter to Two Harbors stockholders, it stated the company might consider an adjustment to its default election mechanism. For example, smaller stockholders who hold less than an unspecified maximum number of shares would receive whichever is the higher value between cash or its shares, UWM said.

In a May 11 letter, UWM previously said "We would be open to considering amendments to our terms, including a potential reverse termination fee and modifications to the election mechanism, but we can only do so through open engagement."

But a Keefe, Bruyette & Woods report on UWM said the company changed its opinion to negative on whether the deal makes sense if it were to prevail in its hostile takeover bid and had to pay all-cash.

However, UWM said in a May 13 press release,

Twice Two Harbors has

It should be noted the CrossCountry deal came after Two Harbors had to postpone a meeting to vote on

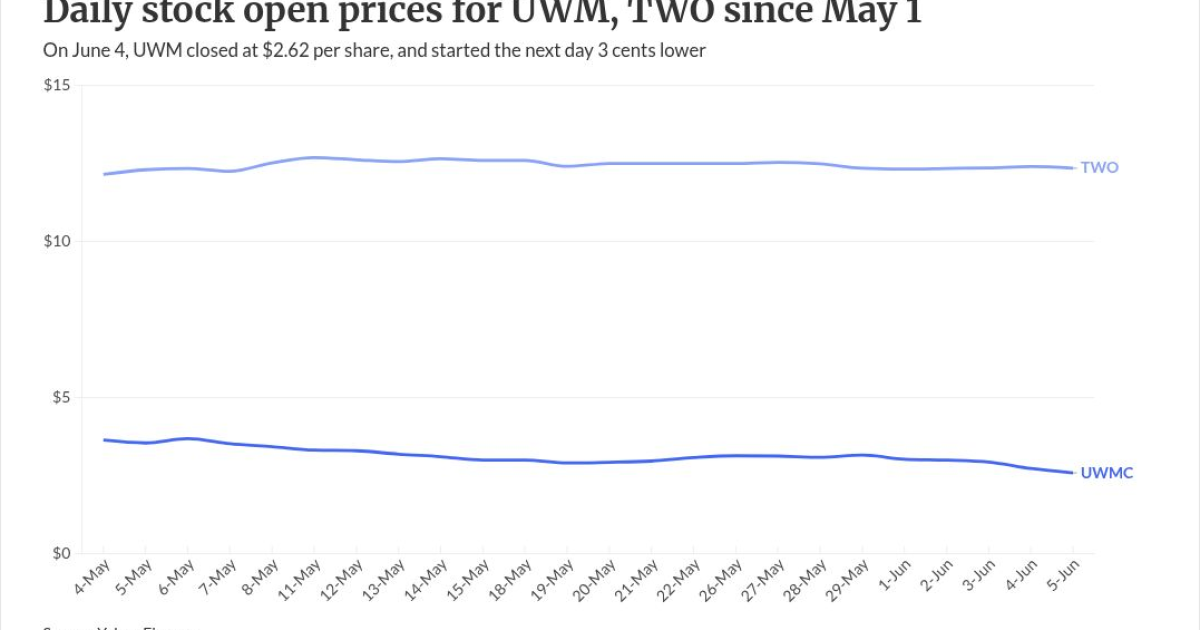

How UWM's stock price is moving

The letter comes at a time when UWM's common stock price has reached all-time lows. It closed on June 4 at $2.62 per share, giving the stock consideration UWM is willing to pay a value of $6.11 per Two Harbors' share, the KBW report calculated.

UWM has not closed above $4 per share since March 10, days before the attempted meeting to have Two Harbors' shareholders approve the deal. On Dec. 17, when

In making its hostile bid, UWM modified its offer to eventually include a $12.50 per share cash option. But, so far, the stock compensation has held to the original 2.3328 UWM shares per Two Harbors share offer.

Why KBW thinks the deal might not be positive for UWM

KBW has come to the conclusion that the Two Harbors deal would no longer be a positive for UWM if it had to pay all-cash for the acquisition, Bose George, an analyst wrote. At the $12.50 per share offer, the price would equate to 1.2 times UWM's book value at its current stock price.

"Any upside would come only if some TWO shareholders default to stock," George said. "So we think the market reaction to a CCM win could be positive."

KBW attributed UWM's stock price woes to investor concerns regarding the nation's No. 1-by-volume lender's high leverage levels as mortgage rates remain elevated.

UWM's long-term debt-to-capital ratio was 3.1 times. Its two largest publicly traded competitors, Rocket and PennyMac Financial Services, have ratios of 1 time and 1.4 times respectively.

"Given the likelihood that mortgage volumes will be lackluster this year, we think leverage is unlikely to improve meaningfully," George wrote.

He believes the only realistic way from UWM to cut leverage is to reduce its dividend. If the company looked

"The company has recently sounded more open to a dividend cut, and we believe that once the TWO acquisition is resolved, a dividend cut is probable," George said. "Despite potential initial share weakness on a dividend cut, we think it is likely to be a meaningful, longer-term positive for capital and valuation."

UWM had no comments beyond what it has said in its press releases and letters. CrossCountry did not have any comment.