Nearly three quarters of lenders expect mortgage volume to improve in 2026, but their confidence is concentrated in refinancings and home equity lending.

Those expectations from the National Mortgage News Predictions 2026 survey, which was fielded online during November and December among 156 mortgage-industry professionals.

More than half, 55% of respondents, work at banks or credit unions and 41% at non-bank lenders. The remainder work at independent or specialty servicers.

Approximately 62% expect volume to increase somewhat, another 15% are of the opinion it would grow substantially. Origination activity being unchanged was the response of 17%.

How economists see the 2026 origination market

Fannie Mae's January forecast predicts originations of $2.4 trillion this year, up from $1.94 trillion in 2025. The

Purchase volume will still make up the lion's share, at an expected $1.49 trillion from $1.38 trillion in 2025.

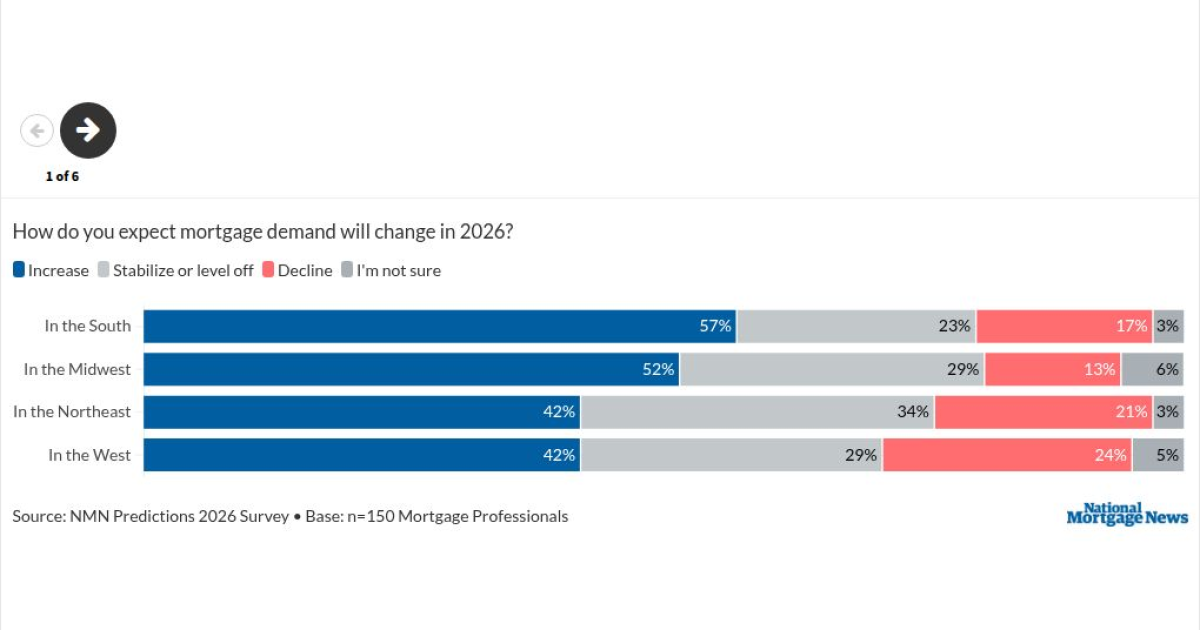

Perspectives on

A majority of southern and midwestern respondents said they thought demand would grow, at 57% and 52% respectively, while 23% and 29% felt it would level off. Just 17% in the South and 13% from the Midwest expect demand to decline.

The Northeast and West survey takers were more balanced in their responses. In each region, 42% said demand would improve. Level off was the response of 34% in the Northeast, with shrink at 21%; in the West, this was 29% and 24%.

"Nonetheless, life events —

"That gradual life-event re-engagement should

What product types do respondents expect to grow in 2026?

Responses around demand for different product types is similar to what is being seen in

Government-guaranteed mortgages — Federal Housing Administration, Veterans Affairs, U.S. Department of Agriculture — have the greatest expectations for growth, with 63% of the survey participants expecting that. This is followed by non-qualified mortgages at 62%. Conforming was next at 57%.

The rate lock data has conforming mortgages with the largest share at 51%, down slightly in December from the prior month and year. Nonconforming, which includes non-QM, made up 17% of December's lock volume, up 141 basis points from 12 months prior.

While FHA locks were down 209 basis points from the previous year, it still made up a healthy 18.9% of the market; VA was at 12.4% and USDA at 0.6%.

While 47% believe reverse mortgage demand will increase in 2026, 22% expected it to level off and 21% predicted less volume. This comes at a time when data indicates

By location, it is the suburbs where respondents had the strongest opinion where demand will increase, at 58%, while 49% predicted rural demand to grow this year and 46% for urban markets.

Products expected to see higher demand this year

While 63% of the respondents said they expect single-family demand to increase this year, in line with the increase in volume expected by Fannie Mae, the surprise might be how many people believe manufactured housing mortgage demand will grow.

Manufactured housing has been mentioned by Trump Administration officials as a tool to improve affordability, but a bill which would have eased lending on these properties was

Lending on

But another type of owner-occupied property also considered to be more affordable,

Where lenders expect the increase in business to come from

An interesting dichotomy exists on the type of buyer mortgage lenders are expecting increased demand to come from. Expectations for the largest growth

Just 37% of originators expect more business from this group, while 29% believe demand will decrease.

By business segment, the origination function is expected to increase by 66%. However, in what might be a pessimistic view of the U.S. economy, a similar number of respondents, 63%, said they