UWM Holdings may have to increase its offer to get the agreed to purchase of Two Harbors over the finish line, industry analysts are speculating.

Two Harbors

But the first sign the deal might be in trouble was on March 9, when

What UWM is doing to get the deal done

A March 16 Securities and Exchange Commission filing from UWM said it hired Okapi Partners to provide strategic advice and assist in the solicitation of proxies. "The TWO Acquisition requires the affirmative vote of the majority of the votes outstanding, and a significant number of stockholders have not yet voted nor submitted proxies," the filing noted.

Okapi will be paid $25,000 for its services upon consummation of the transaction, it added.

Two Harbors

Why analysts are concerned

Both Hagen and Bose George of Keefe, Bruyette & Woods put out separate analyses on the afternoon of March 17 looking at the future path of the transaction.

The effective purchase price UWM would pay for Two Harbors was 23% below the deal's original value, George wrote on March 17..

Two Harbors' shareholders would receive a fixed ratio set at 2.33 UWM shares for each share of the REIT. At the time the deal was announced, it

"If the deal is repriced at the 1.1 times price/book multiple, there could be roughly 30% upside," George said. "Downside is limited: if the deal closes before quarter end with no dividend, there could be around 7% downside since TWO is trading at a 7% premium."

If it closes after the quarter ends, the downside moves to between 4% and 5%, since Two Harbors would pay its normal 34 cents dividend, George continued.

Even if shareholders vote for the deal at the current price but closing happens after quarter end, the downside falls to 4-5% since the company should pay the normal $0.34 1Q25 dividend.

Its shares at the time of the KBW analysis were trading at 0.85 times book value.

Institutional Shareholder Services said Two Harbors stockholders should veto the deal prior to the vote, Hagen noted in his report; NMN sent a message to ISS to confirm.

"It's our expectation for most passive investors tracking [exchange-traded funds] to usually adopt the recommendation of ISS, which has grown to over 20% of TWO's current shareholder base," Hagen said.

He feels the odds are fading for the merger. While the strategic rational remains intact for both companies, it is unclear whether UWM will amend the deal terms to "sweeten the opportunity for TWO shareholders," Hagen wrote.

"We see limited room for UWMC to raise its financial leverage in order to add a cash component to the deal terms," he said. "Even though we think UWMC is highly motivated to see the deal come together, we think it's even more fundamentally critical and relevant from TWO's perspective, considering it needs a scaled origination component to help manage its prepayment risk."

How the deal between TWO and UWM came together

The Two Harbors proxy shows it had three other bidders. All of them bid above tangible book value for the real estate investment trust, the KBW report noted. At least two of those bids were all cash.

"So, given the discount to book value, we think it's possible that other bids re-emerge and/or UWMC raises its offer with TWO shares at 85% of TBV," George said.

Hagen was both optimistic regarding another bidder for Two Harbors, but also restrained in what this would mean.

"If the deal doesn't materialize, we think there's a strong likelihood for a stalking horse to emerge, at the same time we don't expect another buyer will be motivated to offer a higher valuation than the original terms."

UWM first made a proposal to buy Two Harbors on Dec. 9, 2024 at 1.05 times TBV, a chronology in the prospectus said. Two weeks later, on Dec. 26, a bidder only identified as Company A made an all cash offer of $14.25 to $15 per share.

On Jan. 27, UWM made a revised offer set at 1.1 times TBV. In March, Two Harbors made a counter of 1.3 times TBV, which UWM said it was not willing to move forward on, and no further discussions took place at the time.

In August, Two Harbors

But after the agreement was announced, Company C reentered the bidding process but on Dec. 21 pulled out, adding it was not willing to agree to a fixed price per share.

How the stock market is reacting

National Mortgage News reached out to UWM for a comment.

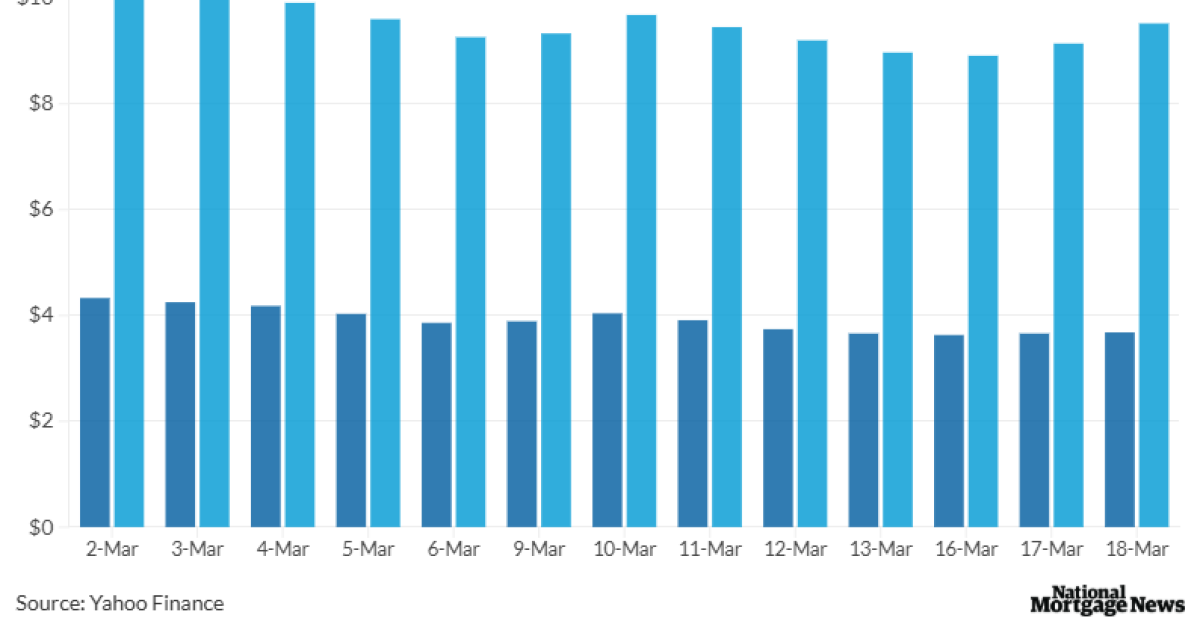

On March 18, UWM closed at $3.68 per share, up 2 cents on the day, but during trading just after opening in the morning was at a 52-week low of $3.59 per share; the high on the day was $3.84 per share around 11 a.m.

Two Harbors also had a wild day of trading, running from a low of $9.08 to a high of $9.90 in the morning before closing at $9.52, up 38 cents.