While both volume and gain-on-sale margins improved year-over-year in the first quarter, discussions between mortgage lenders and Boston Consulting Group revealed a heightened focus on artificial intelligence-driven transformations to permanently manage costs, strategic management company said.

Consolidation is also on the table as a way to scale operations.

The company's quarterly report tracks 10 banks and six independent mortgage bankers, all publicly traded. As a group, while volume was down 11%

For the first quarter, total volume for this group was $210 billion, versus $236 billion in the fourth quarter and $150 billion for the period ended March 31, 2025. The data includes home equity volume, BCG said.

Margin shifts in the first quarter

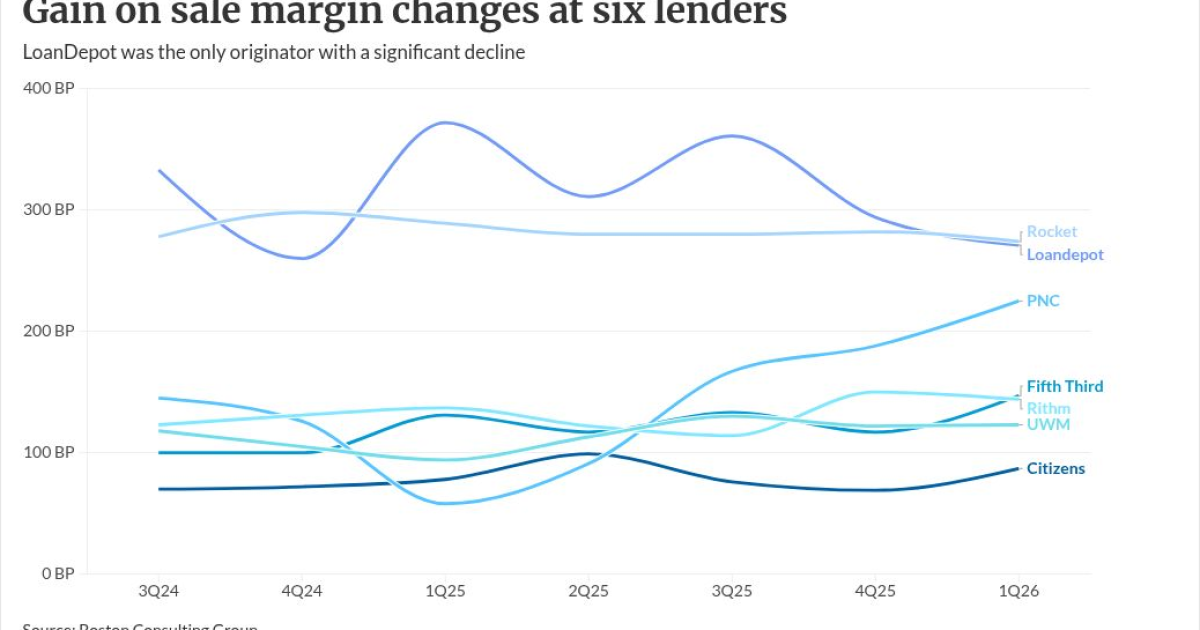

Gain-on-sale data was available for only seven of the companies, of which four had bigger margins versus three months prior. They reported a median increase of 1 basis point from the fourth quarter and 9 basis points for the first quarter of 2025.

Those with the largest increase quarter-to-quarter in GOS were PNC, up 37 basis points and Fifth Third, up 30 basis points. But LoanDepot had a 23 basis point drop off versus the fourth quarter and a 101 basis point decline from the prior year. Still at 271 basis points, it had the second highest margin in the group, trailing Rocket at 274 basis points.

But for the period, BCG said LoanDepot got all of its production from the higher margin retail channel (it announced

What clients are telling BCG about their businesses

Clients are looking at mergers and acquisitions in order to create growth for scale, BCG said. The biggest consolidation play happening in the mortgage industry right now is the battle between

"Faced with rapidly declining origination volumes, companies are evaluating their current strategic investments," the report said. Some of the peers have "tempered" their production expectations for 2026, as mortgage rates which spent the first two months of the year trending lower, rose due to inflationary pressures brought on by the Iran conflict.

At the end of March from four weeks' prior,

What these companies are looking for, BCG said, are:

- To make exits and divestitures from underperforming segments;

- Make

targeted acquisitions of companies within their core business; and - To diversify and expand outside mortgage.

If anything, these firms are looking at finding the last sources of efficiencies as part of "a final push" to right-size their businesses.

How AI fits in its clients' goals

AI will be a key component in making the customer journey transformation. "Cost per loan and efficient customer acquisition will continue to be a source of competitive advantage for those who get it right," BCG said.

In the origination process, its clients are piloting GenAI, looking to

Meanwhile in servicing, these lenders are

"Servicers are exploring operating models centered around agentic AI to [manage] costs via self-help, self-heal, and pre-emptive models of client engagement," the report said. "Our experience shows that these models both reduce costs and improve CX [customer experience]."

Call centers are about 30% of the non-default servicing operational costs at lenders, BCG said.

From its own surveys and discussions, it found three challenges:

- Increasing interaction volumes and complexity of systems and processes are straining mortgage servicers' customer service;

- Economic challenges are leading to a reduction in cost-to-serve, which in turn creates pressure on total and per-interaction costs; and

- Customer expectations for 24/7 instant, seamless and high-quality service are increasing.

A c-level survey found GenAI is scaling fast in response, BCG said, with 90% of organizations piloting or scaling this in customer service. Furthermore, 87% plan to boost their AI and GenAI investments over the next one-to-two years.BCG said its clients are reporting a 65% case deflection rate via the use of chatbots (as part of pre-emptive and proactive resolutions of problems. They also have a 40% reduction in their customer service team and a 10% return on total investment by the third year.

How AI will be the differentiator

Besides the use for pre-emptive and proactive resolution, four other items separate the great companies from the good ones in this area, including having a customer experience so great they want to use it.

Having employees who are "ready, willing and able to use AI." The fourth is having technology which works across channels and layers, along with cross-functional execution which is tight.

The next frontier in getting from good to great is in the areas of pre-emption and self-healing. AI will have to be leveraged in order to stop issues and requests from arising in the first place. It should proactively address issues and requests even before the customer notices them, BCG said.