Mortgage activity picked back up after a one-week dip, despite rising interest rates, according to the Mortgage Bankers Association.

The MBA’s Market Composite Index, which measures new loan activity based on surveys of the organization’s members, jumped a seasonally adjusted 12% for the weekly period ending Jan. 28. Compared to the same week last year, though, seasonally adjusted volumes came in 37% lower.

Activity increased for both purchases and refinances, even as 30-year interest rates continued to climb upward to start the year. The seasonally adjusted Purchase Index increased 4% from the previous week, but volumes were down by 6.7% when compared to the seven-day period of 2021.

The Refinance Index surged 18% higher in the seven-day reporting period, after falling for four consecutive weeks. Renewed activity was driven mainly by a 22% jump in conventional applications, said Joel Kan, MBA’s Associate Vice President of Economic and Industry Forecasting, but overall refinance numbers were still 50% below their level from one year ago,

“There has likely been some recent volatility in application counts due to holiday-impacted weeks, as well as from borrowers trying to secure a refinance before rates go even higher,” Kan said in a press release.

The share of refinance activity relative to total mortgage volume also increased last week, accounting for 57.3% of all applications, compared to 55.8% the previous week. Meanwhile, adjustable-rate mortgages took a 4.5% share of total volume, edging up from 4.4% a week earlier.

The latest survey results come just as TransUnion released its 2021 fourth-quarter credit industry insights report, and similarly found refinance volumes falling significantly in the latter half of last year. According to the report, originations decreased in the third quarter by 13% on an annual basis, driven by a 42% decline in rate-and-term refinances. Cash-out refinance activity increased by 14%, though, while purchase originations remained flat.

“With the pool of consumers who would benefit from a refinance shrinking and interest rates starting to rise, mortgage lenders will now look to implement diversified growth strategies,” said Joe Mellman, senior vice president and mortgage business leader at TransUnion.

Recent forecasts from Freddie Mac and Fannie Mae anticipate refinances to slow further, but purchase originations may make up for some of that slack in 2022. Demand for new home purchases remained robust through the winter but below the previous year’s levels.

Evidence of the strong home-buying demand can still be seen in average loan amounts reported by the MBA, which have steadily risen over the past year. “Stubbornly low inventory levels and swift home-price growth continue to push average loan sizes higher,” Kan said.

The increase in conventional-loan activity helped drive up average loan sizes in the past week to $365,300, up by 0.7% from $362,700 seven days earlier. The mean size of refinances also crept up 0.7% week over week to $308,700 from $306,700, while the average purchase loan size jumped again and hit another survey record. The average came in at $441,400, rising 1.8% from $433,500 the week prior.

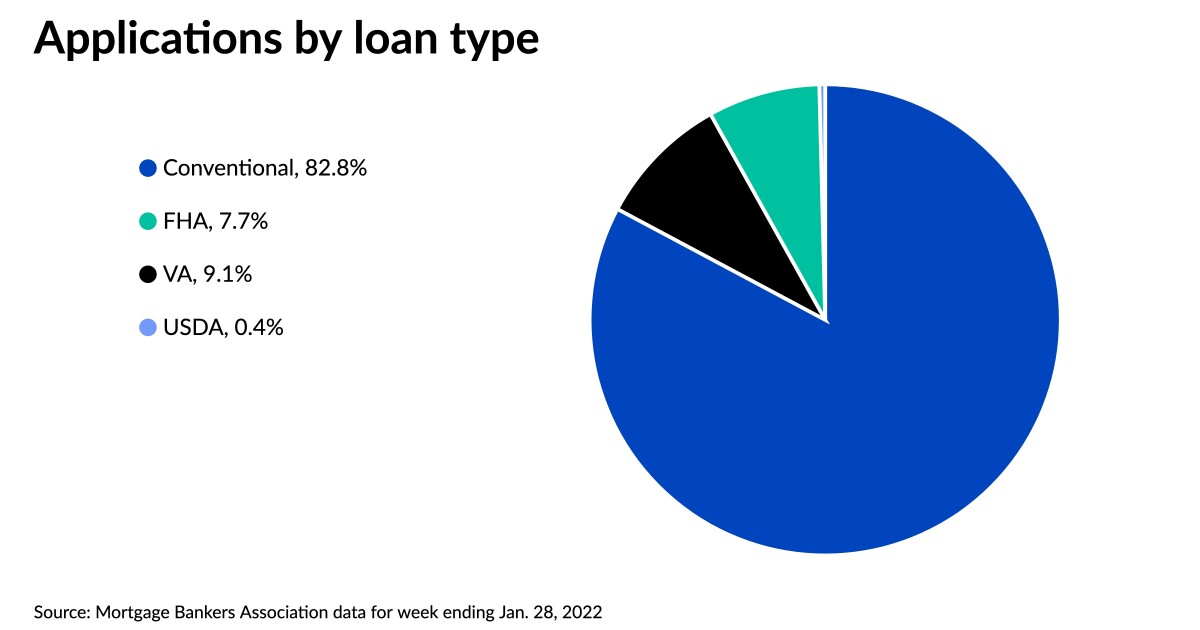

As the number of conventional loans rose, the percentage of government-backed applications relative to overall activity shrank for a second consecutive week, with loans backed by the Federal Housing Administration decreasing to 7.7% of volume from 8.6%. Veterans Affairs-sponsored applications dropped to a 9.1% share from 9.9%, while loans taken through U.S. Department of Agriculture programs edged down to 0.4% from 0.5% the prior week.

Even as prices rise in the current purchase market, Mellman emphasized that the mortgage industry still needs to explore efforts to reach new consumers in order to better compete in the changing market.

“New consumer populations, such as the low-to-moderate income consumer segment, have been relatively untapped,” he said. “Consumer demand for a home is still high, and with more consumers eyeing home purchases, it can be a lucrative avenue for mortgage lenders to pursue in the year ahead.”

Interest rates continued their 2022 surge, according to the MBA, with fixed averages all coming in higher for the fourth week in a row, but the adjustable mortgage rate headed downward.

The contract interest rate for 30-year fixed mortgages with conforming balances of $647,200 or less increased by six basis points to 3.78%, up from 3.72% a week earlier.

The average contract rate of 30-year jumbo fixed-rate mortgages with nonconforming balances exceeding $647,200 rose on a weekly basis to 3.59% from 3.56%.

The contract interest rate of 30-year fixed FHA-backed loans jumped 20 basis points to average 3.89% for the week compared to 3.69% seven days earlier.

The 15-year fixed-rate mortgage averaged edged up a single basis point to 3.01% after coming in the previous week at 3%.

The 5-year adjustable-rate mortgage headed downward for the first time in four weeks, averaging 3.09%, a 9-basis-point drop from 3.18% the previous week.