The Veterans Affairs mortgage benefit got high marks in a survey of current and past military members, but more than half still have at a minimum one misconception about the program.

NewDay USA, which specializes in serving this community, commissioned the online survey of 1,238 people conducted by Researchscape between Feb. 18 and March 7; all of the respondents were current (12% active duty, 20% reservist) or past servicemembers.

The survey was done just before

"These survey results reinforce that there is a real opportunity to reach more veterans with clear information about what the VA benefit offers," said Brian Montgomery, the former two-time federal housing commissioner who

Among those surveyed, 61% currently own a home, while 51% said they at one point in their lives had purchased a home.

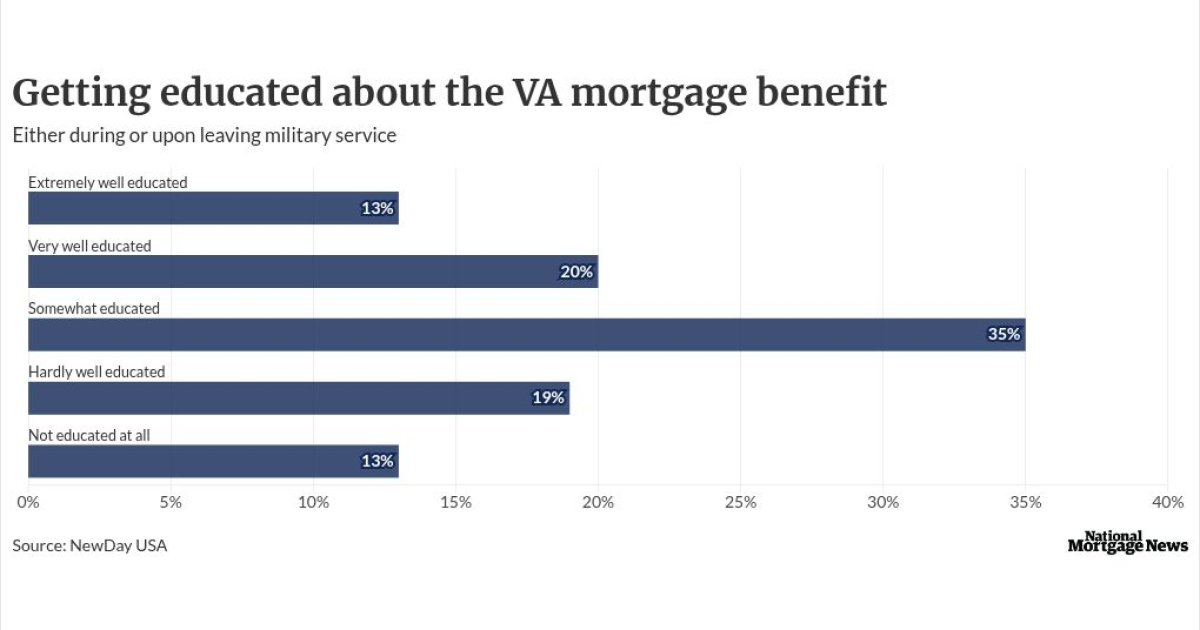

How much do veterans know about the benefit?

When asked about whether they

Of the 629 respondents who purchased a home with financing, 54% used their VA benefit. The survey form allowed respondents to make more than one choice here because of the way the question was worded (the type of financing you ever used to buy a home).

Just under half of those who used the VA program said they could not have been able to buy their home without the 100% financing it provides. Nearly all said they were satisfied in some fashion with their experience.

However, many program users perceived some challenges during the process.

With users allowed to pick more than one response, 26% cited delays in loan approval or processing, while 25% claimed they were confused or had a lack of knowledge about their eligibility for the benefit. Meanwhile, 24% claimed they had difficulty understanding the documentation or program requirements. Having difficulty finding a lender familiar with the VA program was the response of 19%, while 13% felt they did not get enough communication from their lender. The property not qualifying under VA guidelines was listed by 23%.

On the good news side, 38% of the 339 people who answered this question said their process was smooth, so they had no complaints.

Do military families plan to buy a home this year

Of the 750 respondents who do not currently own a home, just 9% said they were completely likely and 12% very likely to buy one this year if they needed to come up with a down payment and closing costs.

This grew to 25% somewhat likely, 26% hardly likely and 28% not at all likely.

Without having to come up with both, 16% responded completely likely, 24% very likely and 28% somewhat likely; just 18% replied hardly likely and 14% not at all likely.

For military families, like their civilian counterparts, rising home prices was cited as the biggest barrier to homeownership, by 62%, followed by income at 55%. Saving for any upfront costs was third at 49%, while debt obligations was the response of 35% and concerns about their credit score, 32%.

Meanwhile 24% said a lack of awareness about their available benefits was a barrier.

Only 58% said they were eligible for the VA benefit, with 30% unsure. When asked if the program requires a down payment, unsure was the top response at 38%, while yes got 30%.

Just under half were unsure if the program

What share of borrowers are looking for VA loans right now

For the week ended April 10, 15.7% of submitted mortgage applications were for the VA program, down from 16.1% the prior week, the Mortgage Bankers Association said. In comparison, conventional increased to 65.1%, a gain of 1.5 percentage points; the FHA share fell to 18.2% from 19.3%, with USDA remaining at 0.5%.

In March, the MBA

- Align minimum property requirements with Fannie Mae and Freddie Mac;

- Reform

the Interest Rate Reduction Refinance Loan program , to improve its effectiveness and ensure it reflects today's mortgage market; - Modernize the allowable fee schedule structure which VA mortgage servicers can charge to process assumable loans; and,

- Align the agency's fee documentation requirements with how third-party services are actually billed and documented.

Lee also called on the VA to change its draft delinquency waterfall proposal to not require borrowers to agree to a monthly payment increase before getting home retention options which do not require them to pay more. The group also wants VA to allow servicers to offer forbearance so the homeowner does not have to commit to a repayment options before their hardship ends.