Half of all mortgage lending is dominated by just a handful of lenders, with 2025 trends showing improving business conditions, but a still-uneven recovery from the housing slowdown earlier this decade.

The

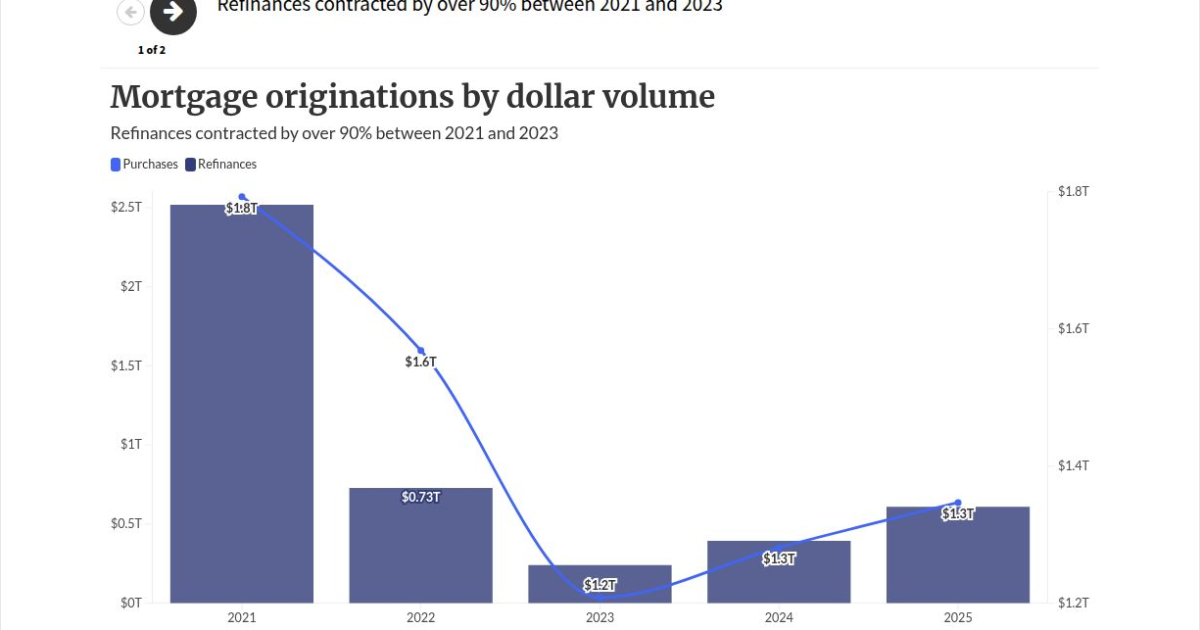

Total originations surpassed $2.12 trillion last year, growing 1.7% from $1.82 trillion in 2024, according to IEmergent's business intelligence database. On a unit count, newly originated mortgages increased to 6.7 million transactions from 6.1 million.

"Growth is being driven by specific products, borrower segments and geographies, while competitive gains are concentrated among lenders with the scale and strategy to capture them," said IEmergent CEO Laird Nossuli in a press release.

Concentration at the top means the ability to scale and develop workflow efficiencies are playing a large role in determining who takes the lead in mortgage lending, according to the analysis. The comments underscore observations over the past several months from tech experts, who have said companies able to

"Understanding where those opportunities exist is critical for lenders planning their next phase of growth," Nossuli continued.

IMBs drive 2025 growth

IMBs also increased their share of market originations to 57.8% on a unit basis compared to 55.8% in 2024, with last year's IMB activity equaling 61.9% of the dollar total.

Meanwhile, the $3.03 billion dollars in originations growth seen in 2025 came primarily through elevated IMB activity, with nonbanks contributing $193 billion to the increase in production, or 63.7% of the overall upswing.

What numbers say about the housing market

Refinances made up 29% of originations, surging from the 22% share in 2024, and formed the foundation for much of last year's higher numbers.

Lenders were more likely to see refis coming out of coastal markets, where they represented as much as 40% or 38% of activity in Los Angeles and San Diego. Elsewhere, though, such as in Texas Sun Belt communities, purchases reigned, accounting for 71% of mortgage transactions in Houston and 68% in Austin, emphasizing the need for individual market strategies.

The average refinance loan size also leaped a notable 14% year to year to $311,200 from $272,900, according to HMDA data. The growth outpaced the 3.1% uptick for purchases, which rose to $379,600 from $368,100.

Upwardly trending loan amounts in both categories indicate housing affordability dictated activity last year, with the need for higher origination amounts a sign of inventory constraints and stretched price levels for many buyers, IEmergent noted.