Late payments on mortgages inched up by 1.76% on a consecutive-month basis in February to more than 1.78 million, marking the first time since May of last year that delinquencies have increased, Black Knight found.

Overall delinquencies, excluding foreclosures and including forbearance, rose to 3.36% from 3.30% due to a 97,000 increase in borrowers with new late payments. The increase was driven by an uptick in early-stage delinquencies that outpaced a 72,000 drop in payments 90 or more days past due.

The slight increase in new late payments may have stemmed from higher mortgage rates, rollbacks in pandemic-related relief, which were expected to normalize loan performance, and geographic concentrations of overdue loans. In states like Mississippi, for example, the delinquency rate was more than twice as high as the national average. However, February’s national delinquency rate was still in line with monthly pre-pandemic levels.

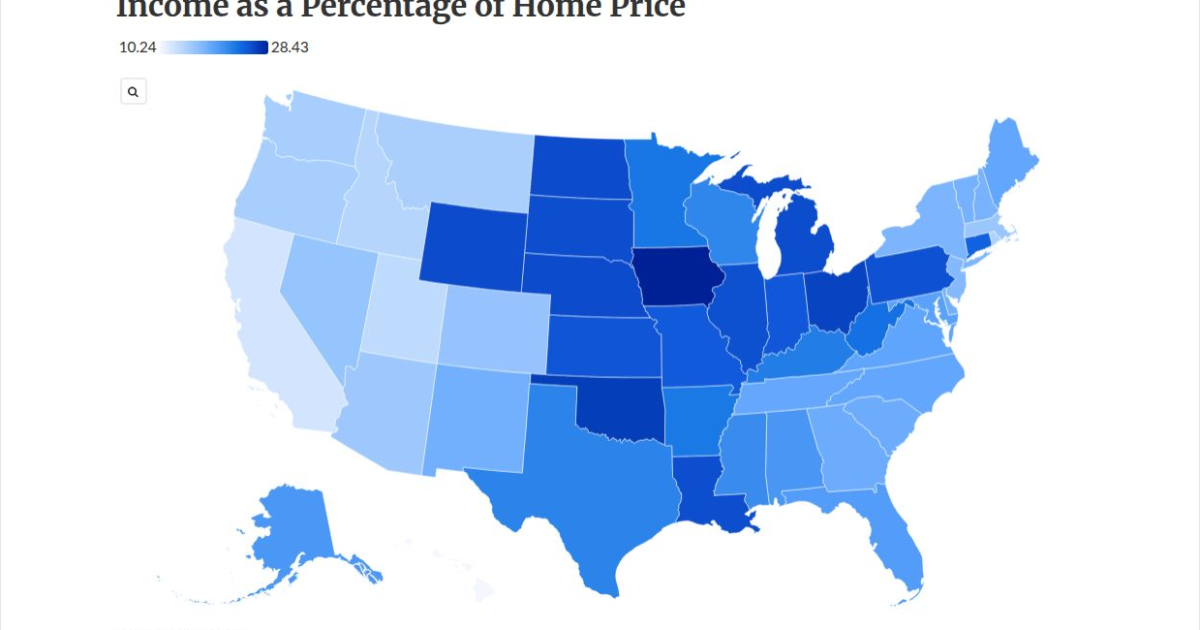

Higher rates have made it more difficult for existing borrowers to lower their costs and have increased financing expenses for home purchases, but economic strength could sustain lending if the gap between wages and housing prices doesn’t widen too severely.

Reduced refinancing drove the monthly prepayment rate in February down by 10.85% on a consecutive-month basis and 60.68% year-over-year to 1.12%, according to Black Knight. The refinanceable universe has shrunk severely, the company found in a separate report. The latest increase in Freddie Mac’s weekly mortgage rate left a little over 2 million people in the market refinanceable, down 80% from the start of the year and 50% in March alone.

The Federal Housing Finance Agency’s fourth-quarter report on foreclosure prevention and refinancing, which also was released Wednesday, recorded similar trends.

The refinancing of loans sold to government-sponsored enterprises Fannie Mae and Freddie Mac inched down on a consecutive-quarter basis to roughly 1.27 million from 1.29 million. During the same time period, payments that were late by 30 to 59 days rose 231,650 from 218,294, and serious delinquencies more than 90 days late fell to 364,294 from 469,650.

Fannie and Freddie loans, which represent one of the largest segments of the mortgage market, tend to have relatively low delinquency rates. The GSEs’ serious delinquency rate in the fourth quarter was 1.19%, down from 1.55% in the previous fiscal period. Their delinquency rate for loans overdue by 30 to 59 days was just 0.76%, up slightly from 0.73% the previous quarter.

In line with a February report from a bank regulator earlier this week, the FHFA found that a relatively high percentage of mortgage holders were aggressive in how they modified loans to offer distressed borrowers payment relief. Nearly half of all modifications completed during the fourth quarter reduced payments by more than 20%, according to the FHFA. For 2021 as a whole, roughly one-third of all modifications lowered the rate for borrowers and generally also extended the loan term or applied other affordability measures.

Deferrals, in which payments suspended for pandemic-related hardships are pushed to the end of the loan and borrowers resume normal monthly obligations, remained the most common home retention action at Fannie and Freddie in the fourth quarter. More than 100,000 deferrals were recorded during the fiscal period, compared to 31,891 forbearance plans, 16,913 modifications and 1,859 repayment plans.