Household debt inched up to another record high in the first quarter even though nonmortgage-related debt drifted lower with a seasonal decrease in credit card balances due in part to tax refunds.

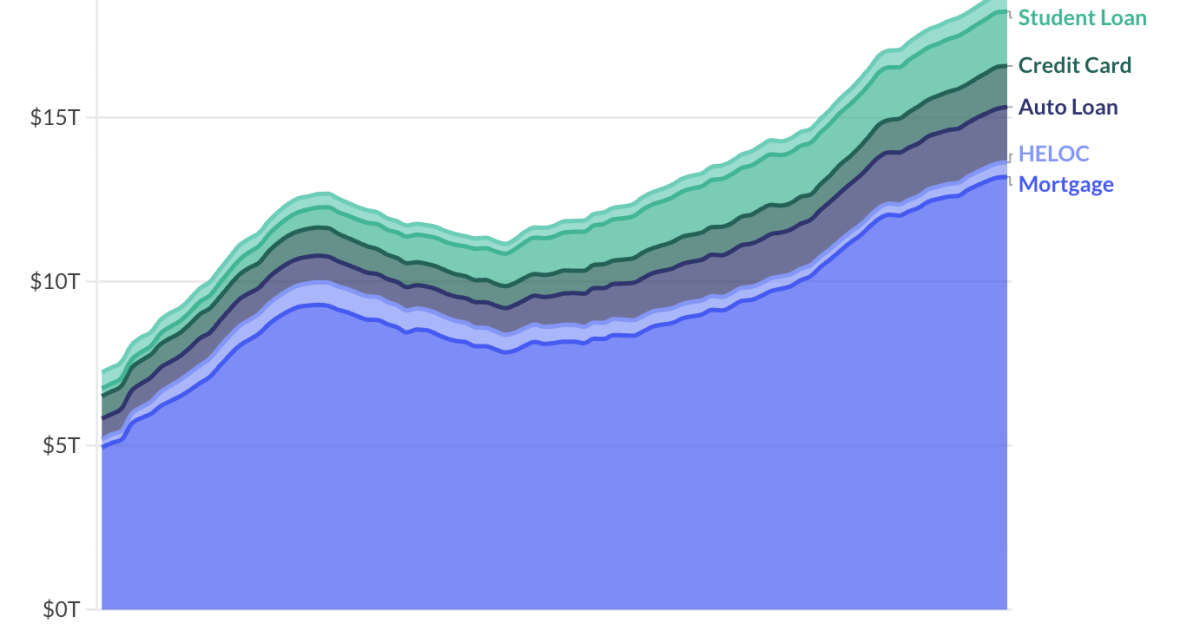

Housing finance obligations rose, driving total debt up by $18 billion to $18.8 trillion during the period, according to an analysis the Federal Reserve Bank of New York's Microeconomic Data Center conducts using an anonymized sample of Equifax data.

Mortgage balances were up by $21 billion, bringing the total in that category to $13.9 billion. Home equity lines of credit rose by $12 billion to $446 billion. Declines in the balances of credit cards and some other types of obligations outside the housing sector offset the gains.

Total delinquencies were generally stable but some mortgage variations shed some light on

Where the mortgage risks are

Overall, serious delinquency transitions for mortgages only "accelerated slightly" from 1.4% to 1.5% during the period, according to the New York Fed's report. Moves into more short-term arrears drifted lower.

Pockets of servicing risk lie within the broader delinquency rate, Selma Hepp, chief economist at Cotality, said in an interview at NMN's offices. She pointed to recent originations in certain markets as well as the FHA rule as reasons for these concerns.

Servicers with such loans are "constantly worrying about how over leveraged their portfolio is, how much they have to do in modifying these mortgages, how little equity they have; or, if they bought on top of the market, now they're finding themselves in negative equity," she said.

Hepp stressed that

"It's not a large increase, but it is concentrated, and it's concentrated in these markets that have seen some price corrections, like Texas and Florida," she said.

Between these concerns and the broader pickup in long-term arrears noted in the New York Fed's report, servicers may have to ramp up their resources for dealing with distressed home inventory in certain parts of their portfolios.

"This is something to watch and could lead to a pick up in foreclosures," Bill McBride wrote in his Calculated Risk blog, commenting on the increase in mortgages' serious delinquency rate.

The former technology executive's reports are closely read because was among the first to foresee a housing bubble that forced government-sponsored enterprises Fannie Mae and Freddie Mac into conservatorship in 2008.

These risks are specific to the mortgage market, but there also are some near-term consumer credit concerns outside the market that could have implications for residential real-estate finance.

Other consumer credit concerns

The New York Fed report flags high serious delinquencies in some other sectors like

"Many households increasingly relied on revolving debt to manage higher everyday living costs during the inflation surge and are now struggling to keep up with repayment," the NAHB economists wrote.

How much and what type of impact this will have on mortgages remains to be seen. It may be contributing to the increase in HELOC debt, which has been ongoing for 16 consecutive quarters.

Credit score distribution supports the notion that mortgage underwriting is doing more to protect the market than it did during the period leading up to the 2008 bubble, with virtually no originations with scores below 620 and "few below 660," according to McBride.

However, he noted that there have been more mortgages originated to borrowers with scores of 660 or higher recently.

"There has been an increase in originations for borrowers in the 660 to 670 range. A significant majority of recent originations have been to borrowers with a credit score about 760," McBride wrote.

While mortgage lenders look at debt-to-income levels and credit scores at origination, the servicing impact that occurs down the road if these worsen may be confirmed fastest for those who encourage borrower communication, particularly for loans with other potential stressors.

"You may not know unless your borrower calls you and claims hardship," Hepp said.