Increased volume in non-qualified mortgage securitization activity is being supported by the growth of "fumbo" loans — fake jumbo mortgages — this week's report from Bank of America Securities said.

The non-agency portion of the report said non-QM production is on track to

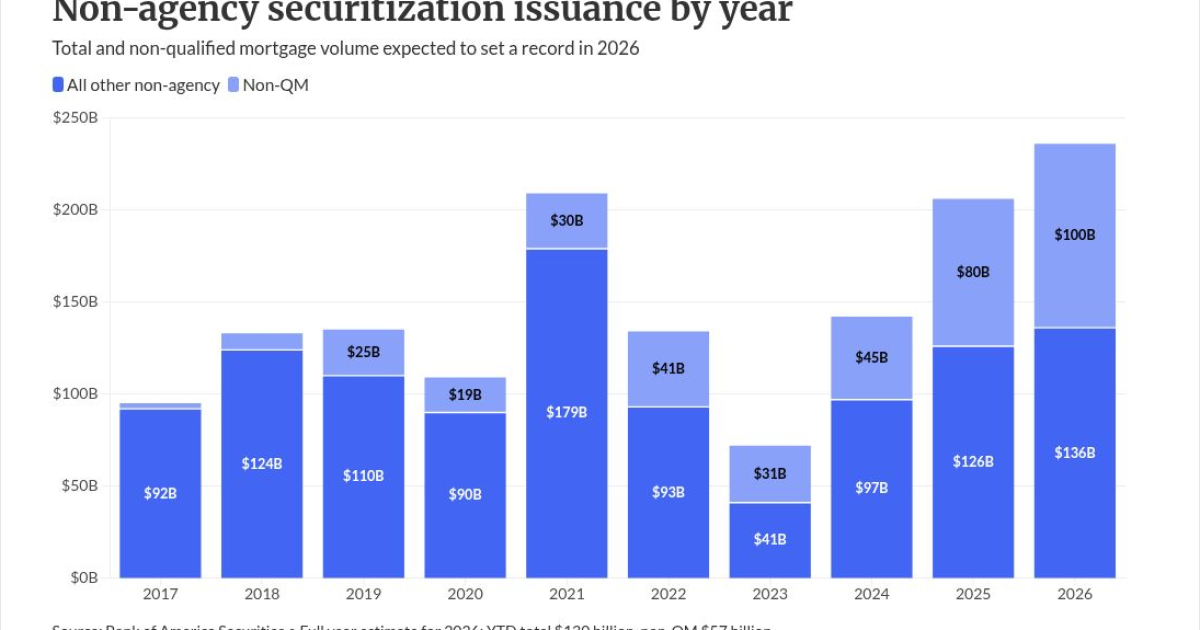

This compares with total non-QM originations of $100 billion, with $80 billion securitized during 2025.

Increased

New jargon enters the mortgage business

The report introduced a new term, "fumbo," into an industry already full of jargon.

"One aspect of the increased volumes within the non-QM securitization channel were attributed to high quality, jumbo-like mortgages being securitized by some of the issuers," the BofA report noted. "We do see an increased share of high-balance loans being included within non-QM deals."

Loans with balances over $1 million made up 28% of this year's new originations, while loans over $1.5 billion had a 15% share. Mortgages that would otherwise meet the criteria for Jumbo 2.0 deals are now taking up a higher proportion of non-QM transactions.

"We note though such loans can have a higher level of delinquency and also exhibit worse convexity," the report said about the fumbos. Some agency-focused originators have highlighted growing non-QM volumes in their business as agency mortgage production slows down.

Investor loans make up 50% of non-QM production. Within that cohort, loans written to borrower credit make up 10%, while 40% are DSCR mortgages. "We thus think that the 10% portion could be a proxy for agency-eligible investor loans (or near miss) which is also coming within the non-QM market," the analysts said.

Why non-QM is gaining volume

There are several reasons for deciding to go the non-QM route, including

"What this means for investors, is that non-QM behaving more like jumbo; lower delinquencies, and higher prepays. but retain non-QM like tail risks," BofA Securities said. "Higher FICO score borrowers have better financing options, combined with larger loans incentivize greater prepays, which will come into effect all the more in a falling rate environment."

The analysts do point out that jumbo-like mortgages could result in lower delinquency rates for the non-QM transactions. In general, non-QM delinquencies have been improving due to better underwriting.

Why investors should be concerned

"Investors ought to watch out for tail risks as these jumbo-like loans may drive up deal-level averages without actually improving the riskiest part of the capital stack," the report warns.

Issuance for the past week of all forms of non-agency securitizations was approximately $4 billion, bringing the year-to-date total to $130 billion.

Spreads widened slightly over the week, with non-QM AAA rated deals at 120 basis points.