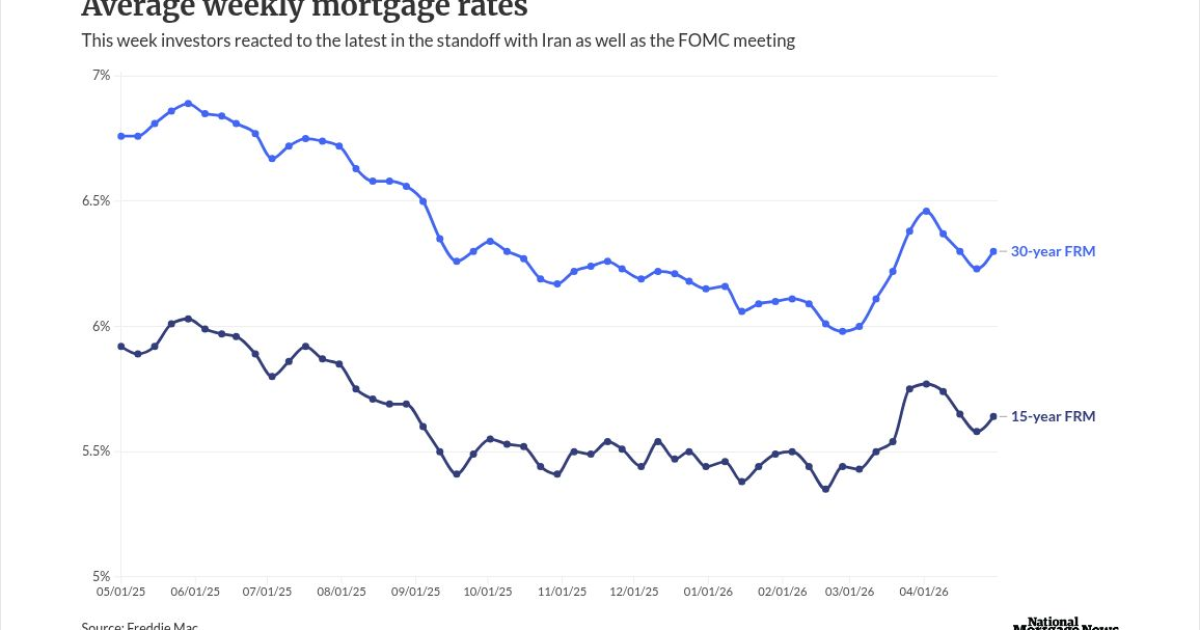

Mortgage rates ended their three-week slide, with the 30-year fixed moving 7 basis points higher as a primary benchmark for pricing loans remained elevated.

For the first time in a month, the 10-year Treasury yield moved over 4.4% on April 29. Other than that late March rise, the last time it was this high was at the start of August.

The last time the 10-year was under 4.3% was a week ago.

The 30-year FRM averaged 6.3% on April 30,

Meanwhile, the 15-year FRM had an average 5.64% for this week, compared with 5.58% seven days prior. For

How the spring purchase market is doing

Higher rates have not affected purchase demand, with these applications rising to over 20% versus one year ago, said Sam Khater, Freddie Mac chief economist in a press release.

"It is clear that purchase demand continues to hold up as prospective buyers react to both modestly lower rates and more inventory to choose from than the last few years," said Khater.

Even though the most recent Mortgage Bankers Association's Weekly Application Survey pointed to purchase demand remaining strong, Lisa Sturtevant, chief economist for Bright MLS, had a different take.

Buyers are remaining tentative, pointing to pending home sales 1.1% lower in April than March, she said in a commentary regarding the Freddie Mac report.

"There are some signs of life among buyers as pending sales have inched up ever so slightly over the past four weeks," Sturtevant said. "But the fact remains that we are not going to see rates fall below 6% anytime soon, and the spring housing market is going to be much more subdued than forecasts suggested at the end of last year."

Purchase application volume on an unadjusted basis was up 21% over the prior year, the MBA reported. Conforming, jumbo and 15-year FRM rates all increased 2 basis points week-to-week, while Federal Housing Administration mortgage rates dropped 1 basis point.

"After a brief pause, in part because of the elevated geopolitical uncertainties, potential homebuyers certainly appear to be moving forward this spring and taking advantage of the more favorable inventory conditions in most parts of the country," MBA Chief Economist Mike Fratantoni said in a press release.

The April FOMC meeting's impact on mortgage rates

April 29 was the day the Federal Reserve,

Even though the move was expected, the 10-year's high on the day was 4.43% before closing at just under 4.42%. As of 11 a.m. on Thursday morning, it was at 4.39%.

However,

Mortgage rates did move a bit higher, with most of this coming in the last 24 hours, said Kate Wood, NerdWallet's lending expert in a statement sent out Thursday morning.

This is a result of "two big movers," Wood said, the first being the standoff in the Strait of Hormuz. "It's not clear if either side will flinch, but the longer this standoff continues, the more its economic consequences will ripple outward," she continued.

Next is the Federal Open Market Committee's decision, but not the vote itself to keep short-term rates unchanged.

"What markets took note of was the level of dissension around the direction of future rate adjustments," Wood explained. "A single word was at issue, but with the Federal Reserve that can be a strong enough signal to move markets — and mortgage rates."

For mortgages, the FOMC's actions or inactions carry significant influence about how markets interpret the overall economic conditions, said Stephen Kates, Bankrate's financial analyst.

"A cautious Federal Reserve outlook contributes to more conservative lending standards through tighter risk management, higher rates, and wider spreads between the highest and lowest offered rates," Kates said after the FOMC decision.

"Due to a mix of lender incentives, marketplace complexity and consumer behavior, borrowers may not find their optimal mortgage rate without investing the time and effort to uncover it through rigorous lender comparisons and improvements to their eligibility."

Everyone is getting more used to uncertainty and by itself is making it less of an obstacle for the purchase market, Sturtevant commented.

"The spring housing market will be characterized by a resetting of expectations," she said. "Both buyers and sellers are accepting that mortgage rates will remain above 6%."