Mortgage Q&A: “How many mortgage quotes should I get?”

When it comes to getting the best deal on your mortgage, you can never shop too much.

Just like any other product you may comparison shop for, the more time you put in, the better deal you’ll probably receive.

Sure, it’s a pain in the you know what, but you’re not shopping for a plasma TV.

This is your mortgage, most likely one of the largest financial decisions you’ll make in your life.

And one that can affect your pocketbook for years and years to come depending on how long you keep it.

So not spending a considerable amount of time shopping for one would be very ill advised. Don’t be one of the many individuals who obtains just one mortgage quote!

Look At Mortgage Rates Online and Track Weekly Averages

- There’s no specific number of quotes needed to score the best deal

- But the more mortgage quotes you receive the better your odds of finding that low rate

- A study from Freddie Mac found that even two quotes as opposed to one can save you thousands over the loan term

- And 5+ quotes from different lenders has the ability to save you even more

These days, we’ve got the luxury of using the Internet to comparison shop.

Back when, you had to scour the phonebook and make phone call after phone call to check on prices and availability.

I remember doing this to buy a pair of high-tops when I was around 10-years old.

I spent a considerable amount of time trying to track down a pair at the lowest price, phoning up dozens of different shoe stores.

To be honest, I can’t even remember if I got the shoes, but I certainly put in the necessary legwork to ensure I wouldn’t overpay. And those were just shoes…

Nowadays, a simple click of the mouse will allow you do most of that tedious work, though you’ll still have to vet the broker or lender after the fact to make sure the quote is legit and they’re a reliable source.

I recommend checking as many channels as possible to see where mortgage rates are currently pricing.

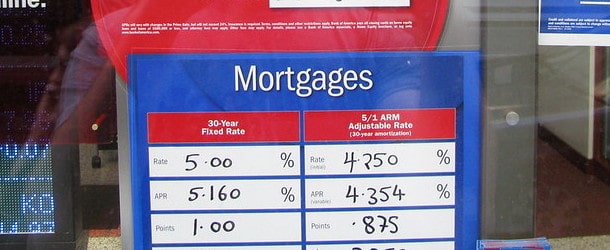

You can check out today’s mortgage rates from a variety of online lenders, as well as look up weekly averages from the Mortgage Bankers Association (MBA), Freddie Mac, Bankrate, and also Zillow.

Watch them for a few weeks to get a good idea as to how they move and why. But note that they are just averages in most cases, not necessarily a perfect science or ultimately what you’ll receive.

And because mortgage rates can change daily, they may be a little outdated. But they’re still worthwhile to track market averages over time.

Once you have a better idea of what most banks and mortgage lenders are charging for everyday loan scenarios, you’ll need to decide on a loan program as well.

Do you want the standard 30-year fixed, or are you a little more daring and thinking an adjustable-rate mortgage could suit you better?

Knowing which product you’re after will make your search a lot easier, though you can still narrow it down to a couple products and rate shop accordingly.

Calls Banks, Mortgage Brokers, Credit Unions, Online Lenders, You Name It

- There are plenty of options to gather mortgage quotes

- Including your own bank, credit union, or competing banks

- Along with independent mortgage brokers and mortgage bankers

- And a slew of online mortgage lenders that make the process quick and easy

Assuming you followed step one above, you should know what most banks and lenders are charging for a typical loan scenario for a variety of home loan programs.

Great! Now it’s time to get your hands on real mortgage rate quotes.

You may be in for a surprise, as those rates you see or hear on TV are often either best case scenario or simply advertising rates aimed at drawing you in.

For example, the rates you see on TV or online may be for a borrower with an 800 credit score and a 40% down payment on an owner-occupied single-family residence. Oh, and a couple mortgage points must be paid at closing too.

Of course, your loan scenario may not be so “vanilla,” so the mortgage rate your quoted could shock you somewhat.

Fret not though; this is why you’re mortgage rate shopping to begin with.

If you’d like, you could start with your local bank or credit union just to get your feet wet. You know, the company where you have your checking and/or savings account.

They probably know the most about you, so they’ll be able to give you a Loan Estimate or pre-approval letter pretty easily to determine how much you can afford and at what rate.

Typically, they offer discounts to existing customers who agree to things like automatic billpay, knowing you’re good for that mortgage payment every month because of the money you’ve got in their bank.

Of course, a lot of times they probably won’t offer the best deal, even with some of those perks thrown in because they’re a big name.

So don’t stop there. Find a mortgage broker or two (I recommend three) and get rate quotes from them as well. See how they stack up against your bank/credit union and go from there.

A broker can shop rates on your behalf, which cuts out some of the legwork, but you still need to compare mortgage brokers too!

Then check out the countless online mortgage lenders out there, many of which won’t be household names.

While you may not have heard of them, there’s a decent chance they can offer lower mortgage rates due to that lack of advertising and the reduced overhead.

If you’re comfortable working with a mortgage lender remotely, they could offer a much better deal than the brick-and-mortar, big name shops.

[Why are mortgage rates different?]

Negotiate, Negotiate, Negotiate Once You Collect Your Quotes

- The beauty of multiple mortgage quotes is you create competition

- It gives you the real ability to negotiate your rate and fees

- Without another quote to compare it to you won’t have much of an argument

- Other than begging or ignoring them until they agree to lower their price

The beauty of receiving multiple rate quotes is that you can negotiate. With just one, there’s not much you can do aside from asking/pleading for a lower rate. Well, you can lie too.

But if you’ve got multiple companies vying for your precious business, you can pit them against each other until one comes out on top by offering the lowest rate with the best terms.

Additionally, there are mortgage lender that offer low-rate guarantees, so having other quotes in hand could help you land those deals.

You’ll also grow more confident as you discuss rates and fees with multiple lenders, learning the mortgage lingo as you go.

This should aid in negotiating more effectively if you actually know what you’re talking about and aren’t fooled by the nonsense they’re spouting.

Just be sure to look at all the details when comparing offers, including all costs (lender and third-party fees), the interest rate, and the APR.

It’s not always easy to get an apples-to-apples comparison, so you may actually have to do some math to choose the best deal.

And remember, while price is definitely important, you need a competent bank or broker with the ability to close your home loan!

I know, the whole process is annoying, but as mentioned earlier, this is a huge financial decision, so a little homework can go a long way.

Those who put in the time and effort might get their money’s worth, potentially tenfold.

Read more: 10 Ways to Save Money on Your Next Mortgage