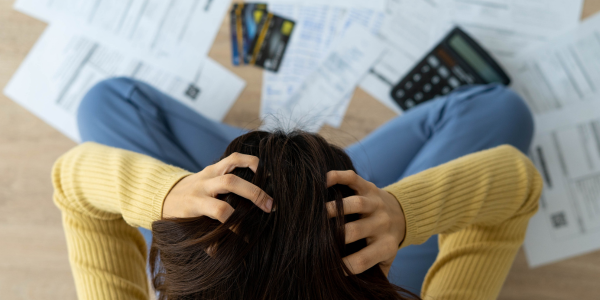

Rising interest rates and economic uncertainty have left many homeowners feeling the pinch, with some struggling to keep up with their mortgage repayments. While mortgage stress levels remain relatively low, according to Reserve Bank data, the number of overdue mortgages is on the rise. If you’re concerned about servicing your mortgage, it’s important to know that you have options. Here are three strategies that could help ease mortgage pressure.

1. Switch to interest-only payments

Switching to an interest-only mortgage may be a short-term solution to reduce your mortgage repayments. When you make interest-only payments, you temporarily stop paying down the principal balance of your loan, which can significantly lower your repayment amount.

Pros:

- Lower mortgage repayments could provide immediate financial relief, freeing up cash for other essential expenses.

Cons:

- The principal amount remains unchanged, which means you’re not building equity in your home by paying down your loan.

- Once the interest-only period ends, your repayments could increase as you’ll have less time to pay off the principal loan.

What to watch out for:

Banks usually limit the length of time you can be on interest-only, and they typically don’t extend the overall loan term to compensate. That means you could end up with higher repayments in the future. It’s essential you discuss this option with your lender or mortgage adviser to understand the long-term impact on your finances.

2. Restructure your home loan

Another approach to managing mortgage stress is to restructure your home loan. Restructuring can help you get a better interest rate on your mortgage, new repayment terms, or a longer period to repay your mortgage.

Pros:

- Lower repayments can make your mortgage more affordable, especially during financial hardship.

Cons:

- You could end up paying significantly more in interest over time.

What to watch out for:

While restructuring your home loan can ease immediate financial pressure, it’s important to consider the long-term costs. Before making a decision, use a mortgage calculator to understand the full financial impact and consult with a mortgage adviser to explore the best options for your situation.

3. Take a repayment holiday

If you’re facing short-term financial difficulties, consider applying for a repayment holiday which allows you to pause your mortgage repayments for a set period. However, interest continues to accrue during this time, which means you’ll either need to extend your loan term or increase your repayments once the holiday ends.

Pros:

- Provides immediate relief by pausing mortgage repayments, giving you time to recover from temporary financial setbacks.

Cons:

- Interest continues to accrue, which increases the total amount you owe.

- You could face higher repayments or a longer loan term once the holiday ends.

What to watch out for:

A repayment holiday should be considered a last resort, especially if you’re unsure about your ability to resume repayments once the holiday ends. If your financial situation doesn’t improve, you could end up owing more and still struggling to meet your mortgage obligations. It’s important to assess whether this option will truly provide long-term relief or simply delay the inevitable.

Get help if you’re struggling

If you’re feeling overwhelmed by mortgage stress, don’t hesitate to reach out for help. Banks are required to consider applications for assistance when borrowers experience unexpected changes in their circumstances, so the sooner you ask, the better!

Work with a Mortgage Express mortgage adviser who can provide tailored financial advice and help you navigate your options, ensuring you make informed decisions that best fit your situation. Contact us today to discuss how we can help you manage mortgage stress.