The mortgage securitization market is facing two significant shifts: a proposed regulatory change that could reduce risk weights for private-label MBS, and an industry push for due diligence standards aimed at keeping up with surging growth in second-lien products.

The risk weighting for investment-grade MBS in the private market would fall from 20% to 15% under

Government-sponsored enterprise securitizations' risk weighting would remain at 20%. Securitizations that Ginnie Mae guarantees would retain the 0% risk weighting they have because they are directly backed by the government.

A 'TRID grid' for home equity

Separately, the Structured Finance Association has released recommended due diligence standards for certain integrated disclosures issued under the Truth in Lending and Real Estate Settlement Procedures acts that pertain to home equity products.

The recommended guidelines are based on subcomponents of the "TRID grid" the association first produced in 2016. TRID risk has been a key compliance concern for the secondary market because it carries assignee liability, which means risk related to flaws in the origination process could flow through to investors.

Due diligence firms and rating agencies have referenced the TRID grid as a uniform means of assessing compliance risk in first-lien mortgage securitizations. Third-party review firms use the standards in assigning A through D grades to loans, which ratings agencies then reference.

The new standards create a uniform way to conduct due diligence on a subset of the TRID grid that pertains to second-lien loans. SFA developed uniform TRID guidelines for closed-end seconds in consultation with stakeholders, including regulators, because of how much these types of securitizations have grown in recent years.

"There has been growth in subordinate lien financing and diligence firms don't want to be the bottleneck or get involved in a race to the bottom. So we decided we needed strong, efficient, uniform testing standards that apply to a subset of the TRID grid pertinent to subordinate-lien financing," said Dallin Merrill, head of policy at the Structured Finance Association.

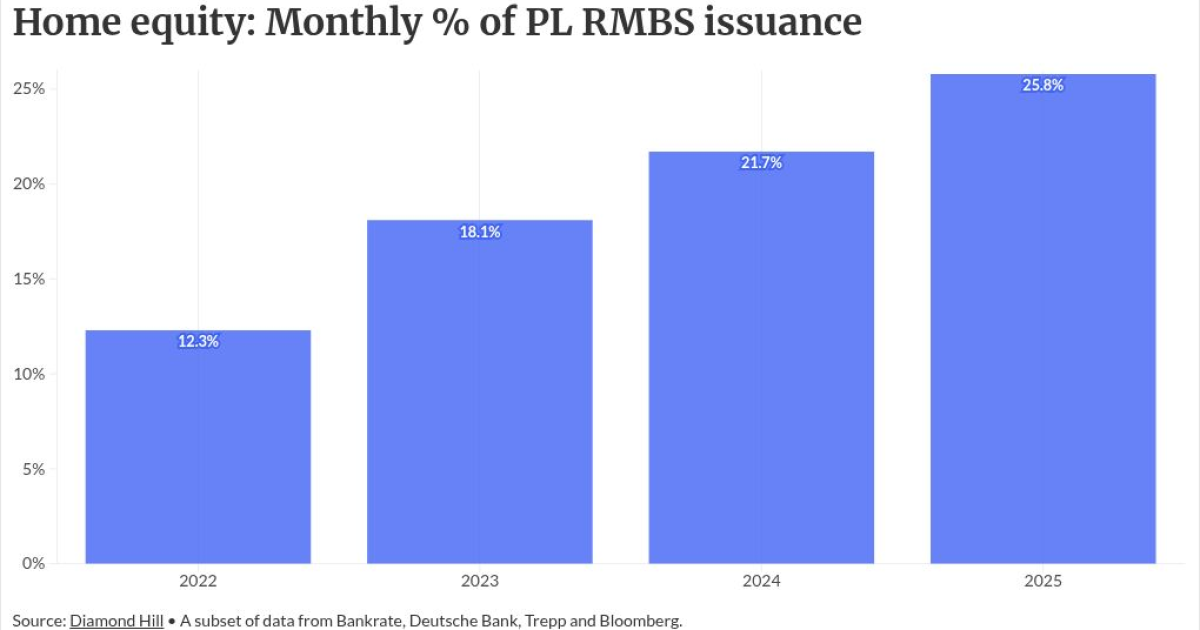

Overall home-equity securitization issuance share per month nearly doubled between 2022 and 2025, according to investment firm Diamond Hill's analysis of third-party data.

Home equity securitization, including CES, made up 12.3% of issuance in 2022 as compared with 25.8% in 2025, according to part of a larger set of third-party statistics on non-agency residential MBS. As of March, the percentage for March was 24.3%. A dip in rates and a short month may have contributed to the leveling off seen earlier this year. Rates have since risen.

More assignee-liability standards coming

The Structured Finance Association also is working on updating its current 4.0 standards for the original TRID grid with a 5.0 version aimed at accounting for changes in the landscape resulting from federal deregulation.

The new TRID grid, which also encompasses other consumer-protection rules that carry assignee liability, may include updates related to

Stakeholders also are looking at the trend toward

SFA additionally seeks to create some standards for how third-party review firms utilize artificial intelligence.

"We're planning to look at how due diligence firms use AI, or at least how it is disclosed," Merrill said.