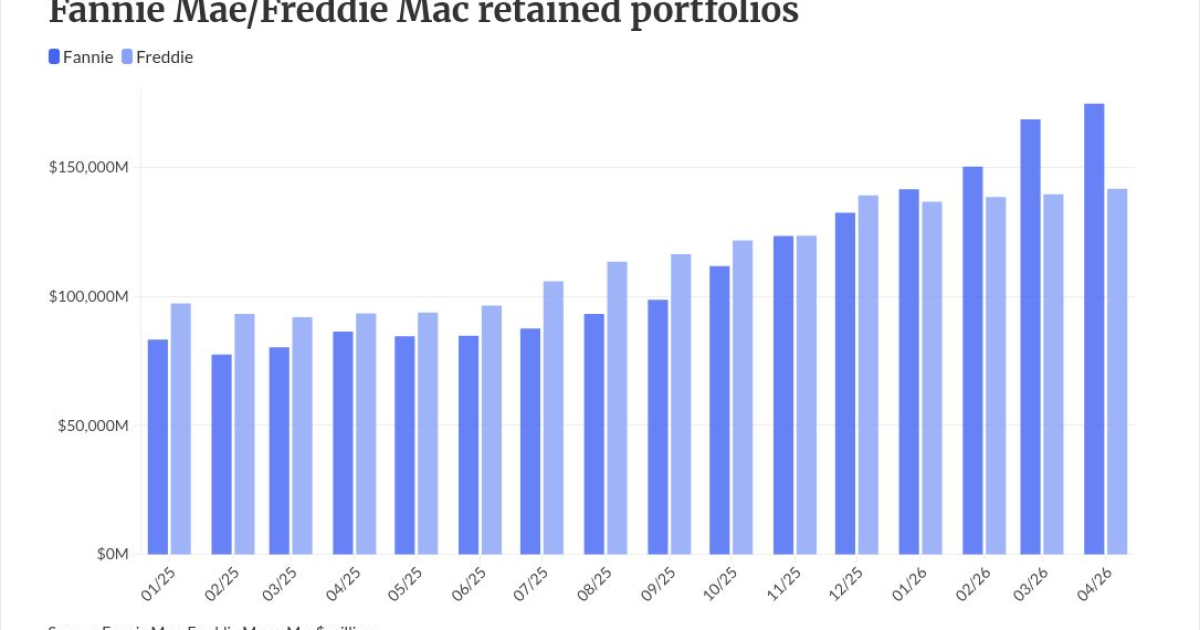

Fannie Mae reclaimed the lead in retained portfolio growth last month, pushing to a new record after a year in which Freddie Mac had outpaced its rival.

Fannie reported that its retained portfolio jumped to $174.84 billion in April from $168.74 billion

While Fannie is back on top when it comes to the retained portfolio, Freddie has held onto a consistent quarterly lead in single-family acquisitions that materialized in 2025.

The GSEs don't typically break out new single-family acquisitions in their monthly reports. Both enterprises also have portfolio limits and do not retain all the loans they acquire for several other reasons related to financial and risk management.

Both portfolio growth and increased competition for new acquisitions have benefits for single-family mortgage lenders. The former helps contain some of the upward pressure on mortgage rates from inflation, and the latter can give lenders more options when it comes to selling loans into the secondary market.

Although mortgage rates in

While current rates are not ideal, the reduction compared to a year ago shows portfolio growth has had an impact, said Rob Zimmer, head of external affairs for the Community Home Lenders of America. CHLA and the Independent Community Bankers of America were among the early advocates for limited portfolio expansion at Fannie and Freddie as a means of lowering rates.

"Washington has had a role in the spread and has been making a difference. We just need them to make more of a difference," he said "It's odd to me that the Freddie portfolio barely budged. There's more work to be done."

Forecasts for the portfolios

Growth in the portfolios will eventually run up against limits but will generally be supportive of book values for agency mortgage investors like real estate investment trusts this year, analysts at Keefe, Bruyette & Woods said in a report published Sunday.

"We would expect GSE buying of agency MBS to continue through 2026 as a tool for supporting mortgage rates, with both portfolios potentially reaching the $250B cap by year-end," Bose George and Frankie Labetti, equity researchers at KBW, wrote.

Mortgage to Treasury spreads that drive rates are narrower than a year ago at levels "modestly above" 200 basis points and a long-run average of 192, according to the KBW analysts.

"We think further spread tightening is likely limited," they wrote.

Zimmer foresees a level below 200 basis points as an achievable goal, depending on what happens in the market more broadly.

"Arguably, we can't control global macroeconomic trends, but that spread needs to get below 200 basis points, and really needs to be around 190," he said.