Government mortgage-backed securities guarantor Ginnie Mae is providing some deadline relief to issuers who may be rushing to file annual audited financial statements this week.

Ginnie has announced that it's removing the 15-day advance notice requirements for extension requests on the statements, which are due March 31 for most issuers. The financial statements must be submitted 90 days after the end of the fiscal year, which typically is Dec. 31.

"Effective immediately, the requirement is that these extension requests must be submitted via the applicable module in Ginnie Mae Central (GMC) on or before the due date," the government guarantor wrote an All Participants Bulletin published late Friday.

The leeway could give issuers more time to deal with changes this year that include a new audit schedules report announced in early March. That report is tied to major capital and

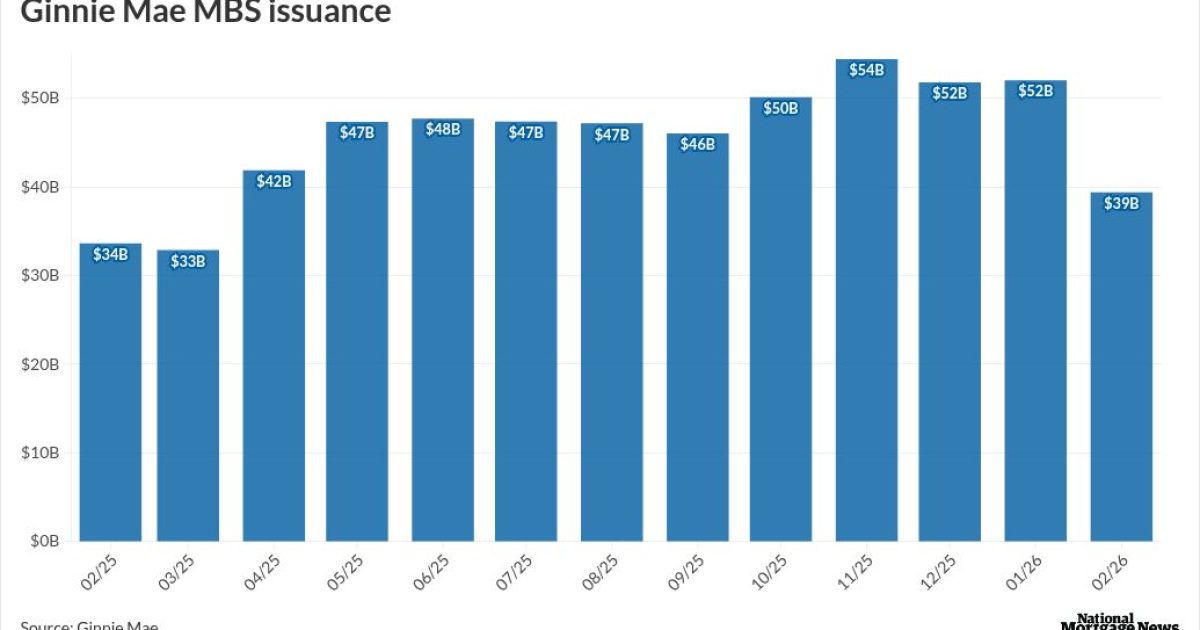

Ginnie Mae issuers collectively have been responsible for roughly $30 billion to $55 billion of new mortgage-backed securities per month for the past year. Ginnie's total portfolio outstanding was more than $2.9 trillion as of February.

Ginnie plans to

Ginnie Mae is also closely monitoring the risk of data breaches. Issuers and document custodians must provide

New prepayment data

Ginnie also announced Friday that it has now fully implemented plans laid out last year to disclose 3-month conditional prepayment rates on all active single-family loan pools with sufficient history to do so.

"By evaluating prepayments over longer horizons, such as a three month rolling average, investors can smooth out month-to-month variability to better reflect the underlying prepayment behavior of a given pool or cohort," Ginnie wrote in a disclosure bulletin published Friday.

Interest rate changes that have a bearing on prepayments have been

Loan-level reporting update

Ginnie additionally is proceeding with plans to speed up its transition in operations aimed at allowing

Several operations beyond servicing will be impacted, including underwriting, securitization and investor reporting.

Gormley said that the progress on this, while relatively faster than in the past, will remain deliberate because the implications of transitioning away from a loan-pool level system are so far reaching.

"This is a fundamental shift in program operations and requires a steady and methodical approach to ensure no disruptions to the Ginnie Mae program," Gormley said.

While there is considerable work involved in the change it also will likely have wide-ranging benefits too, according to Gormley.

"The net effect of this transition will be to provide more precise cash-flow tracking for portfolio managers and investors; more effective prepayment, delinquency and loss mitigation modeling; error reduction and – we believe – lower costs in originations, servicing and securitization," he said.