Application volume for Federal Housing Administration mortgages slowed in May, as did insurance-in-force growth, but the latter is still outpacing private mortgage insurance, an analysis of data by Keefe, Bruyette & Woods found.

Furthermore, mortgage delinquency trends for FHA, which increased meaningfully

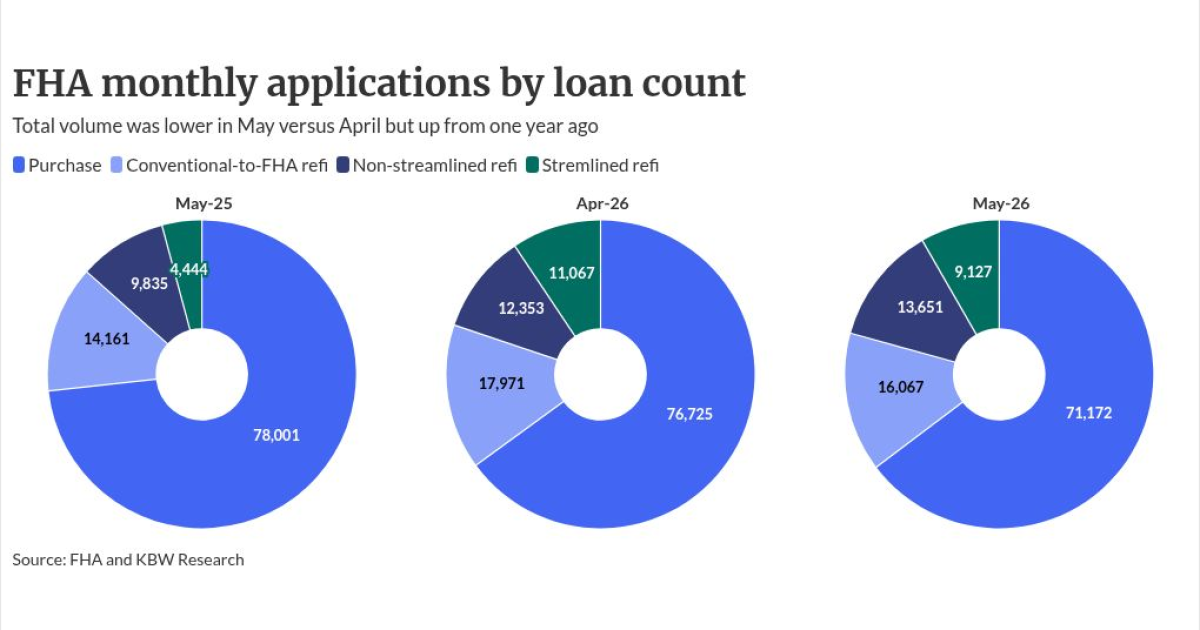

The total number of applications submitted for FHA loans was 107,433, compared with 120,700 in April and 106,441 for May 2025. For purchases only, May's total of 71,172 was lower compared with the prior month's 76,625 and from 78,001 for the previous year.

During May 2025, 14,161 conventional-to-FHA applications were received. Other forms of refinancings, non-streamlined as well as streamlined, were also lower month-to-month, but elevated year-over-year.

Optimal Blue

But nonconforming rate lock share increased to 19.3%.

May's insurance-in-force grew 8.3% at the FHA versus the prior year. However, the pace "ticked down modestly" from the first quarter's 8.8%, George said. April's growth rate was 8.4%, he added.

But the FHA IIF increase pace remains

This compared with $1.616 trillion in the fourth quarter and $1.579 trillion in the first quarter of 2025.

Meanwhile, FHA heavy servicers like PennyMac Financial Services should benefit from the stabilizing delinquency rate for the program, he wrote.

Expectations industry participants expressed during the Mortgage Bankers Association Secondary and Capital Markets Conference in May, were for

In the first quarter,

George sees signs of a shift.

"FHA delinquencies, which increased meaningfully after changes to the FHA modification rules in October, appear to be stabilizing," George said. "While the seriously delinquent bucket remained flat month-to-month and was still up meaningfully year-over-year, both the 30-day and the 60-day buckets fell year-over-year (although they were up month-to-month)."