Mortgage banking units operated by major U.S. homebuilders saw their pre-tax income slide for the period ended March 31, reflecting the significant year-over-year declines in net income for the period ended March 31 was reported at a quartet of U.S. homebuilders.

Some analysts are even warning of

However, some of those who just reported provided positive comments on their performance even in the face of a mortgage rate environment that changed radically during the quarter.

The Mortgage Bankers Association's Builder Application Survey for March bore out some of this optimism. It found

"Last month, mortgage rates rose and economic uncertainty increased, and our estimate of new home sales reached its highest level in four months," Joel Kan, the MBA's deputy chief economist said in an April 14 press release.

"This growth was supported by higher levels of unsold inventory in many markets across the country, some of which were move-in ready and were relatively more appealing to homebuyers who were eager to purchase a home."

On the other hand, the National Association of Home Builders/Wells Fargo sentiment index fell to

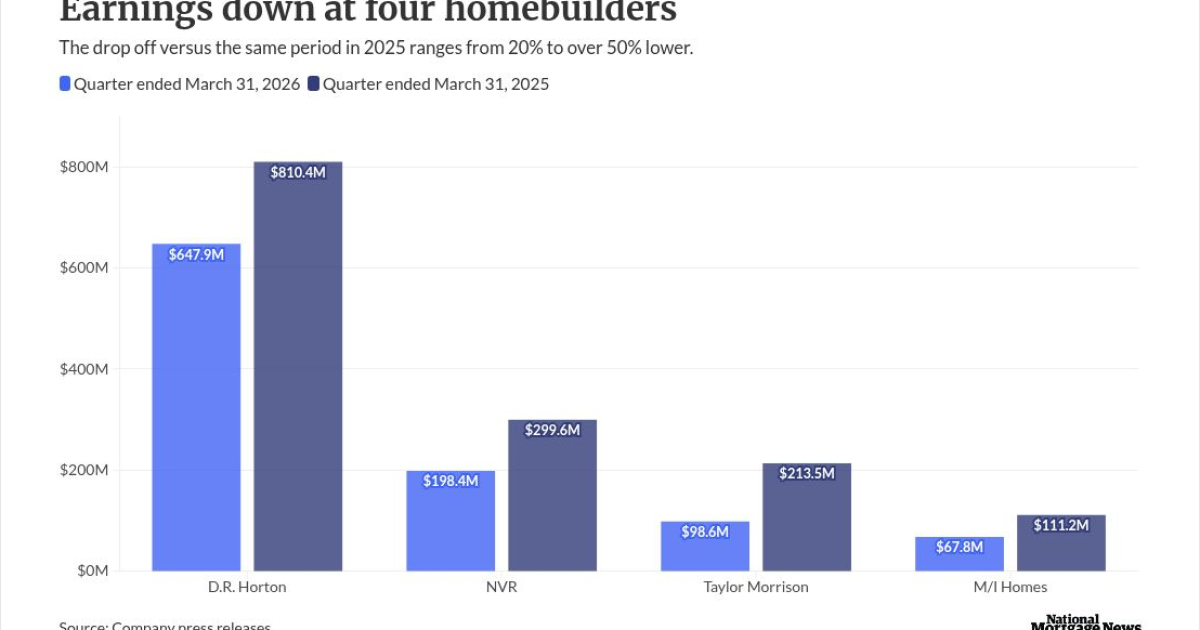

Here is a roundup of earnings from some publicly traded homebuilders whose reporting ended on March 31:

D.R. Horton warns of elevated sales incentives

Net income for the second fiscal quarter attributable to D.R. Horton fell 20% to $647.9 million from $810.4 million

"Affordability constraints and cautious consumer sentiment continue to impact new home demand," said David Auld, executive chairman, in a press release.

Still, the company reported an 11% year‑over‑year increase in net sales orders, while reducing its inventory of unsold completed homes by 35% from a year ago, Auld continued.

Revenue from its homebuilding business for the second fiscal quarter decreased by 2% to $7.1 billion. Homes closed increased 1% to 19,486 homes from the prior year, while the cancellation rate of 16% was in line for the same period in 2025.

Horton's financial services business added revenue of $192.8 million with pre-tax income of $51.7 million, resulting in a pre-tax profit margin of 26.8%.

"We expect our sales incentives to remain elevated in fiscal 2026, with incentive levels dependent on demand, mortgage interest rates and other market conditions," Auld said. "Based on our performance year to date, we remain on track to deliver results within our original fiscal 2026 guidance."

NVR's mortgage pretax income falls 17%

Even as new orders increased at NVR by 7% as compared to a year ago, net income at the homebuilder and mortgage banker was down by 34% for the first quarter.

The company reported net income of $198.4 million for the period ended March 31, versus $299.6 million one year prior.

Homebuilding revenues of $1.83 billion represented a 22% drop from $2.35 billion for the first quarter of 2025. But the average sales price for a new order was just 2% lower, at $440.100.

The first quarter cancellation rate of 14% compared with 16% a year ago.

Its mortgage banking business reported pretax income of $27.1 million, down 17% from the first quarter of 2025, when it earned $32.5 million. NVR's mortgage volume fell 27% year-over-year to $1.05 billion from $1.43 billion. The capture rate fell to 83% from 86%.

Taylor Morrison reduces reliance on incentives

Taylor Morrison Home reported a significant decline in net income for the first quarter, by more than 50%, to $98.63 million from $213.47 million for the same period in 2025.

Its home closing revenue decreased approximately 28% to $1.3 billion. This was driven by a 26% decline in closing volume to 2,268 homes and a 4% decrease in the average closing price to $578,000.

"Encouragingly, our first quarter sales were achieved with a significant increase in the mix of to-be-built orders to 38% from 28% in the fourth quarter, a more than 100 basis point sequential reduction in incentives, and a 30% decline in our finished spec count to 863 homes," said Sheryl Palmer, Taylor Morrison chairman and CEO in a press release. "With net orders outpacing closings, our backlog grew 23% sequentially to 3,465 homes."

Net financial services revenue, which

Its mortgage business' capture rate was 88%, stable with one year ago.

Income down at M/I but still a "very solid" quarter

M/I Homes net income of $67.8 million for the first quarter was down from $111.2 million one year prior, even as company CEO and President Robert Schottenstein called said those numbers were "very solid."

New contracts were up 3% year-over-year, he noted.

"We continue to believe that long-term housing demand is supported by favorable demographic trends and an undersupply of housing," Schottenstein said. "We have a strong financial position with record shareholders' equity of $3.2 billion, cash of $767 million, and no borrowings under our $900 million credit facility."

Financial services revenue at M/I was $31.23 million, relatively flat with the year ago period's $31.52 million.