WASHINGTON — The Federal Deposit Insurance Corp. released a revised economic inclusion strategic plan Thursday, aiming to advance people's personal financial stability by encouraging lending in underserved communities.

The agency's updated blueprint, which comes a decade after the first draft was released, emphasizes four opportunity areas: Creating banking relationships, saving and building credit, developing small business and affordable housing growth and encouraging bank activities in underserved communities.

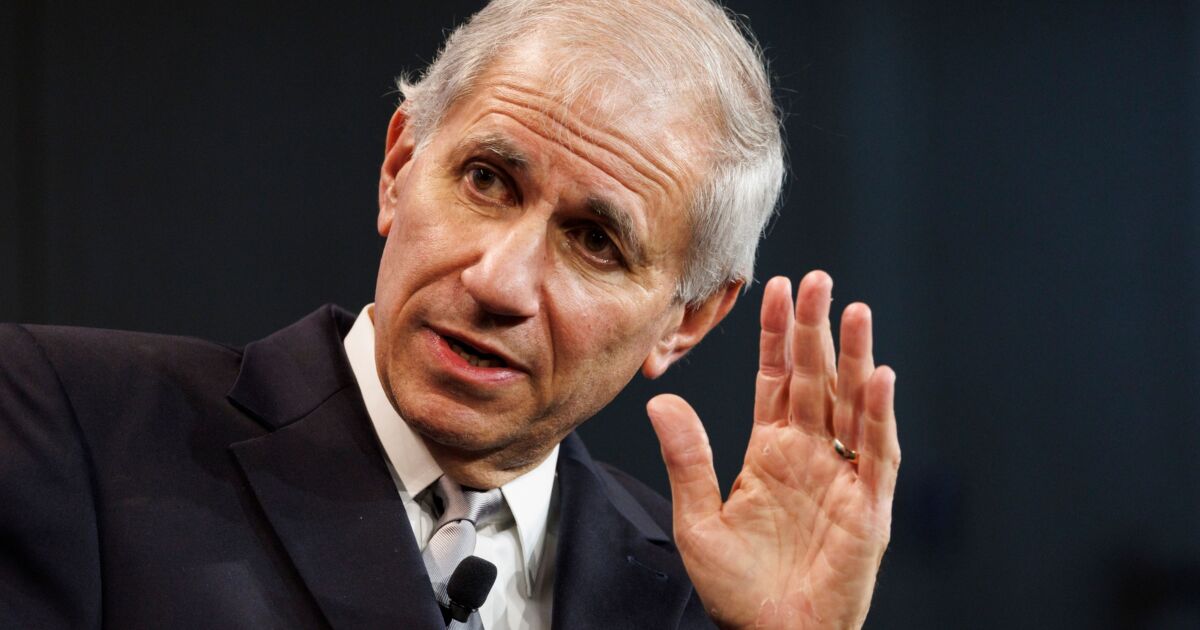

In what FDIC Chair Martin Gruenberg called "the biggest change" to the economic inclusion strategy, the agency will press banks to step up community development initiatives, such as affordable housing, small-business loans and investments in financial institutions that work with minorities, women and low-income populations.

"While the FDIC has long sought to support banks' community development efforts, the explicit connection to its economic inclusion work is new and entirely appropriate," Gruenberg said at the National Community Reinvestment Coalition's annual conference Thursday. "Stated plainly, the plan recognizes that banks are unlikely to succeed in their efforts to build trusted relationships with households if they are otherwise neglecting to make investments that strengthen the communities in which those households live and work."

Jennifer Tescher, president and CEO of Financial Health Network, said the focus on specific outcomes — such as building savings, credit and wealth — is an important amendment to the economic inclusion plan. While rates of unbanked and underbanked households decreased from 28% in 2011 to 18% in 2021, per FDIC data, Tescher said financial security takes more than a bank account.

"What's most notable about this new plan is the focus on outcomes," Tescher said. "I'm really pleased that the FDIC has focused this plan around these four key areas that are critical for achieving financial well-being."

This new plan comes as the FDIC, the Federal Reserve and Office of the Comptroller of the Currency

On Thursday, Gruenberg said the FDIC was "firmly committed to the support" of the new CRA, which he added will help ensure consumers can access needed services affordably, and encourage bank investment in community development financial institutions, minority depository institutions and women's depository institutions.

As part of its revised economic inclusion plan, the FDIC will monitor its progress in driving community development through banks' investment and participation in Community Reinvestment Act-related activities.

Tescher said that the FDIC's new strategy recognizes the important interplay between individual peoples' needs and community needs on financial health.

"In the past, the economic inclusion plan was about people, and CRA was about place," Teacher said. "Now the economic inclusion plan really combines people and place."

Top banking regulators reaffirmed their commitment to bolstering the Community Reinvestment Act despite a court challenge, emphasizing their personal dedication to seeing the rule implemented.

Tescher is a member of the FDIC's advisory committee on economic inclusion, and said her involvement in the development of the agency's new strategic plan was limited to offering feedback on previous drafts and perspective for the updated version.

Last fall, the FDIC's Office of the Inspector General

In his Thursday speech, Gruenberg also highlighted specific financial products that have helped "set the stage" for financial stability and reduce the amount of unbanked households. Accounts designed to limit the risk of overdraft fees weren't widely available a decade ago, Gruenberg said, but are now offered by at least 340 banks. Gruenberg added it's promising to see a rise in banks that offer small-dollar loans, which can provide a path to build good credit and offer an alternative to payday lenders and other nonbanks.

At the NCRC conference, the FDIC chair added that the agency wants to work with groups that represent unbanked and underbanked folks to successfully execute the economic inclusion strategy.

"We recognize that the FDIC will not succeed with a go-it-alone approach," Gruenberg said. "The support of other federal, state and local agencies, of community based organizations, local leaders, bankers, educators and others, is critical."