Freddie Mac reported rates edging downward this week, diverging from Treasurys, as a hot inflation report brought with it higher bond yields and signs of rising housing market pessimism.

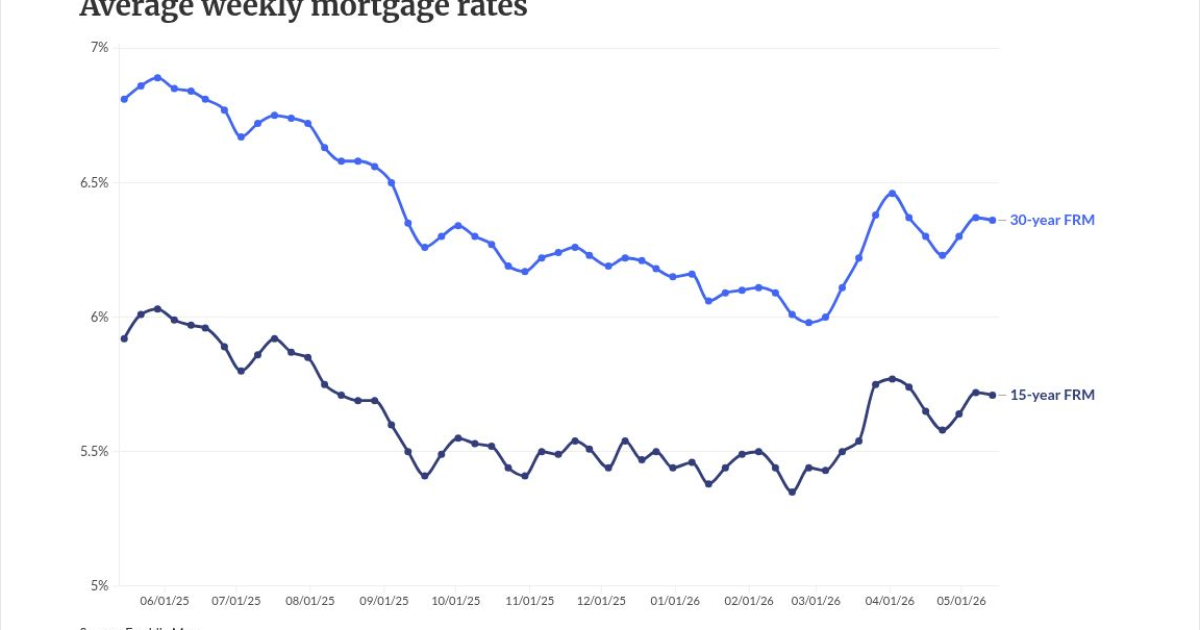

The 30-year fixed rate came in one basis point lower, according to Freddie Mac's Primary Mortgage Market survey of May 14, averaging 6.36%. Rates inched down

Meanwhile, the fixed 15-year dropped at a similar pace, coming in at 5.71% compared to 5.72% in the prior survey period. The current rate is over 20 basis points lower than 5.92% reported in the same week last year.

Freddie Mac's data ran counter to other housing research, which saw the 30-year average tracking in the opposite direction to hit months-long highs after this week's release of the Consumer Price Index.

Lender Price's rate tracker on National Mortgage News' website reported the 30-year fixed average at 6.63% as of Thursday morning, jumping from 6.5% last week. Meanwhile, Optimal Blue's mortgage market index showed the 30-year conforming rate also up to 6.42% Thursday, compared to 6.33% seven days earlier.

While Freddie Mac saw rates essentially flat, its latest numbers indicate averages are still well above their marks prior to the onset of the Iran War. In late February, the government-sponsored enterprise reported the 30-year average at 5.98%, briefly dipping below the 6% threshold for

"Bond market fears that the Iran War would spur inflation were a big component of mortgage rates' rise when the conflict began; seeing those fears borne out is probably bad news for bonds and for rates," said Kate Wood, NerdWallet's home and mortgage expert in a research statement.

Investors responded to the inflation report this week by sending yields for 10-year Treasurys, which typically influence the direction of the 30-year average, higher. After closing at 4.39% on May 7, the 10-year started trading on Thursday at 4.47%.

What this might mean for the housing market in 2026

The impact of the Iran War on rates and overall affordability undeniably threw cold water on mortgage lenders hopes for 2026, quashing early-year momentum and enthusiasm, according to Cotality Chief Economist Selma Hepp.

"A lot of the benefit coming into this year with lower mortgage rates was refi activity, and now that's drying up," she said in an interview with National Mortgage News.

While plenty of pent-up purchase demand exists, current rates also raise questions about sales activity for the coming months, with the recent spike in rates hitting payment-sensitive buyers most acutely.

"This surge in rates changed the dynamics for the spring homebuying season," she said.

Buyers in need of affordability relief may struggle to find it on the interest-rate front, according to Clever Real Estate.

"Buyers have been told for two years that rates would ease, and the April CPI report is another sign that the 'wait for relief' strategy is wearing thin," said Clever President and CEO Ben Mize.

"The numbers point to mortgage rates in the 6.3% to 6.5% range through the rest of 2026, not the sub-6% rates many buyers were hoping for. That changes what a realistic buying budget looks like for a lot of households," he added.

Some encouraging signs also appear

While the Iran War threw a wrench into early-year housing forecasts for 2026, a majority of first-time buyers still remain hopeful about moving into a home, according to a new study from TD Bank this week.

Over 80% of respondents in the TD survey said they were optimistic about the housing market this year, and 55% are creating a homeownership budget. The latest weekly application data from the Mortgage Bankers Association also illustrates consumer demand from some segments determined to relocate or purchase their first home, with

"Purchase activity increased across all loan categories and remained ahead of last year's pace, signaling that buyers are adapting to the current, high-rate environment,"