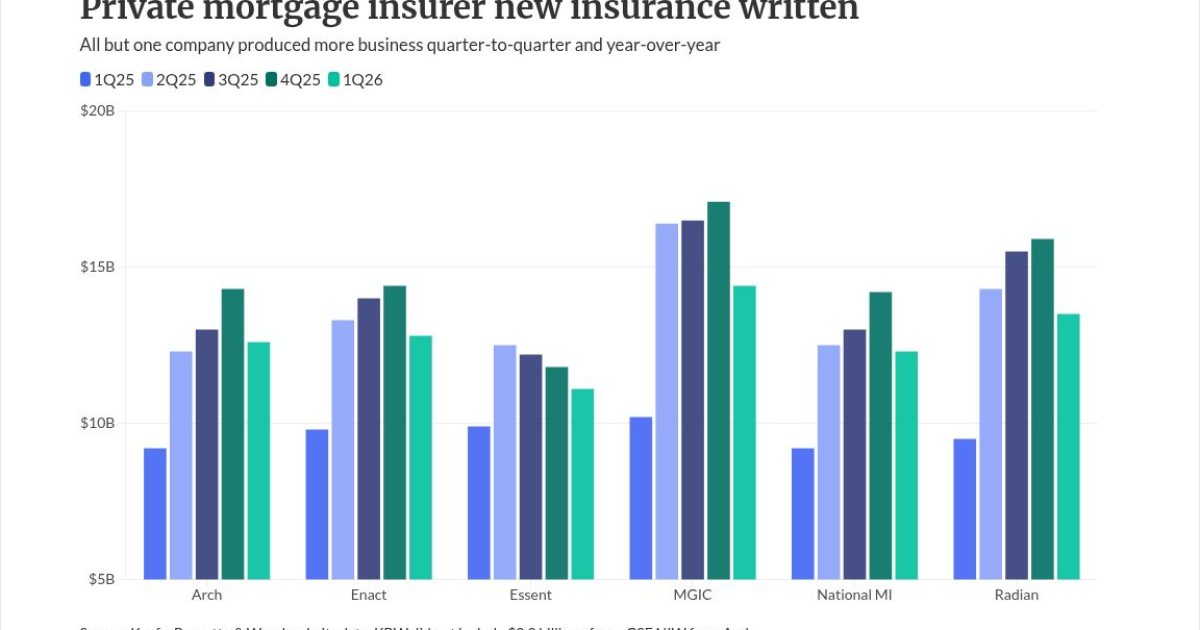

Reflecting both the unusually strong fourth quarter for home loan originations and the volatile rate environment for the period just ended, private mortgage insurers wrote 13% less business versus three months prior.

Still, with mortgage rates going to the low 6% range from near 7% one year ago, the six active underwriters did 32% more volume, Keefe, Bruyette & Woods calculated.

The data is in a note on Essent Group's first quarter results, the final of the six to report for the period.

New insurance written by all of the MIs totaled $76.7 billion in the first quarter. They ended the

All five companies which KBW tracks came in below estimates on NIW.

While the differences in market share narrowed, MGIC and Radian remained at the top of the table and Essent at the bottom.

The following is a roundup of first quarter earnings at the private mortgage insurers:

Large share declines, but MGIC still No. 1

Net income at MGIC Investment totaled $165.3 million for the first quarter. This was down from $169.3 million for the last three months of 2025 and from $185.5 million from the first quarter a year ago.

Meanwhile, the company had the largest percentage decline in new insurance written quarter-to-quarter, down by 16% to $14.4 billion. For the fourth quarter it did $17.1 billion, but in the first quarter of 2025, MGIC had volume of $10.2 billion.

KBW predicted $16.3 billion of NIW for this year's first quarter.

On the earnings call, management was asked how

"Any macroeconomic headwind is something that we're conscious of and something that we think a lot about," Nathan Colson, executive vice president, chief financial officer and chief risk officer said. "To date, I don't think we've seen a lot of direct impact."

In general, when it comes to delinquencies, the industry is coming off of historically good levels and it always expected some normalization to take place, Colson said. In particular, later stage delinquency cure rates are doing much better than before the pandemic.

"It's just the average loan size and thus the average exposure is higher," Colson added in response to another question. "So I think the changing vintage mix just moving closer to today's values is far and away the driver of that increase versus anything you'd see maybe regionally, or anything that we're seeing or changing from an assumption standpoint."

Radian's first results including Inigo

During the first quarter, Radian Group's business model change hit a key milestone, with the

Its net income of $124 million was down from $155 million for the fourth quarter and $145 million for the first quarter of 2025.

Net income from continuing operations was $129 million, versus $159 million and $152 million respectively.

During its period under Radian's ownership, what is now described as the Specialty Segment reported adjusted pretax operating income of $40 million.

"With the addition of Inigo, we now operate across two complementary noncorrelated insurance businesses, each with its own earnings and distinct risk and return dynamics," said Radian Group CEO Rick Thornberry on the earnings call. "We believe this structure expands our growth opportunities and enhances our ability to deploy capital to an attractive risk-adjusted returns."

As for the remaining businesses to be sold, the real estate services and title underwriting and agency, Radian expects the process to be completed by the third quarter.

Radian Guaranty's NIW totaled $13.5 billion for the quarter; this was below KBW's expectations of $15.1 billion.

It had volume of $15.9 billion for the fourth quarter and $9.5 billion for the first quarter last year.

Enact finds consumers remain resilient

Enact Holdings, whose former parent Genworth remains its primary shareholder controlling 81% of the company, reported net income of $168 million for the first quarter.

This was down from $177 million for the prior period, but on a year-over-year basis, a slight increase over $166 million.

Enact had the second smallest percentage drop off versus the fourth quarter but also the second small gain from the first quarter of 2025 in terms of NIW.

It finished the first quarter with $12.8 billion of NIW, down from $14.4 billion three months earlier but up from $9.8 billion a year ago. The KBW prediction for current period new insurance written was for $13.6 billion.

Purchase volume was in line with normal seasonal trends, but low rates early in the first quarter provided a boost to new policies due to refinancings, said Rohit Gupta, president and CEO on the earnings call.

"While the macro environment remains uncertain and inflationary pressures accelerated as gas prices have risen, the consumer continues to show resilience," Gupta said. "Overall, labor market conditions remain supportive and credit performance remains healthy." So far, overall credit trends remain in line with Enact's expectations.

Gupta was asked because the Primary Mortgage Insurer Eligibility Requirements use Classic FICO in setting the standard, would the recent Federal Housing Finance Agency announcement cause those to be revisited as part of the credit score modernization adoption process?

Enact is fully supportive of initiatives which qualify more home-ready consumers, Gupta said, repeating comments he made during the prepared remarks.

"From an implementation perspective, we have been working very constructively with the FHFA and the GSEs to be operationally ready and we stand ready today to operationally implement VantageScore 4.0," Gupta said. It is the items like the PMIERs where Enact and the other mortgage insurers need further guidance and it is waiting for Fannie Mae and Freddie Mac to provide this.

Arch does $2.2 billion non-GSE transaction

The U.S. mortgage insurance business of Arch Capital Group had a non-GSE transaction of $2.2 billion of new insurance written in the first quarter, the company said during the earnings call. Inclusive of this transaction, Arch did $14.8 billion in the first quarter.

But the KBW table is only for policies written for GSE loans. Arch $12.6 billion in the first quarter, compared with $14.3 billion in the fourth quarter and $9.2 billion one year ago.

Arch's mortgage segment, which also includes credit risk transfer and international business, had underwriting income of $221 million for the period. This is down from $250 million in the fourth quarter and $252 million in last year's first quarter.

"Overall, mortgage performance continues to exceed expectations and provide shareholders with a differentiated and diversifying source of earnings that support long-term value creation," Arch Capital CEO Nicolas Papadopoulo said on the call.

Arch Capital reported net income of $1.0 billion, up from $564 million one year ago.

National MI's business trending as expected

In its fourth quarter earnings call, NMI Holdings said it expected volume this year would look similar to how it trended in 2025. This has "absolutely been the case through the first quarter," said Adam Pollitzer, president and CEO, on its earnings call.

Year-over-year the first quarter was better because of the rate environment, especially in January and February.

"Now that they've sold off as we look ahead through the remainder of the year, I think we're still calibrating off of 2025 performance, which, again, was a highly constructive environment, and we'd be delighted to see that type of experience this year," Pollitzer said.

The parent company of National MI finished the quarter with $12.3 billion of NIW, compared with $14.2 billion in the fourth quarter and $9.2 billion one year ago. KBW had expected $13.6 billion.

Net income of $99.3 million, compared with $94.2 million for the fourth quarter and $102.6 million during the first three months of the year.

Essent remains smallest of the MIs

Essent Group reported the smallest percentage decline among the six active underwriters between the fourth and first quarters in terms of NIW. At the same time, it had the smallest year-over-year gain.

It did $11.1 billion in the first quarter, compared with $11.8 billion in the fourth quarter. For the first quarter of 2025, it did $9.9 billion. Expectations from KBW were for $12 billion of NIW.

Net income of $171.8 million was up from $155 million for the fourth quarter, but a little lower than $175.4 million for the first quarter of 2025.

Enact is now the only mortgage insurer actively pursuing the title line, having

"On the title front, we continue to transition the business from a stand-alone operation to an adjacency of our mortgage insurance franchise by leveraging our customer base and providing title solutions," said Mark Casale, chairman, CEO and president. "The coordination between our MI and title teams continues to build momentum in expanding the number of Essent title customers, but we know this business is rate sensitive and results will continue to improve as origination volumes recover."

As for competitive trends in the MI business, Casale said "you are starting to see a little reach here and there." This pricing competition is around the edges, but nothing alarming, he added.