Mortgage originations hit a three-and-a-half-year high in the fourth quarter of last year, as

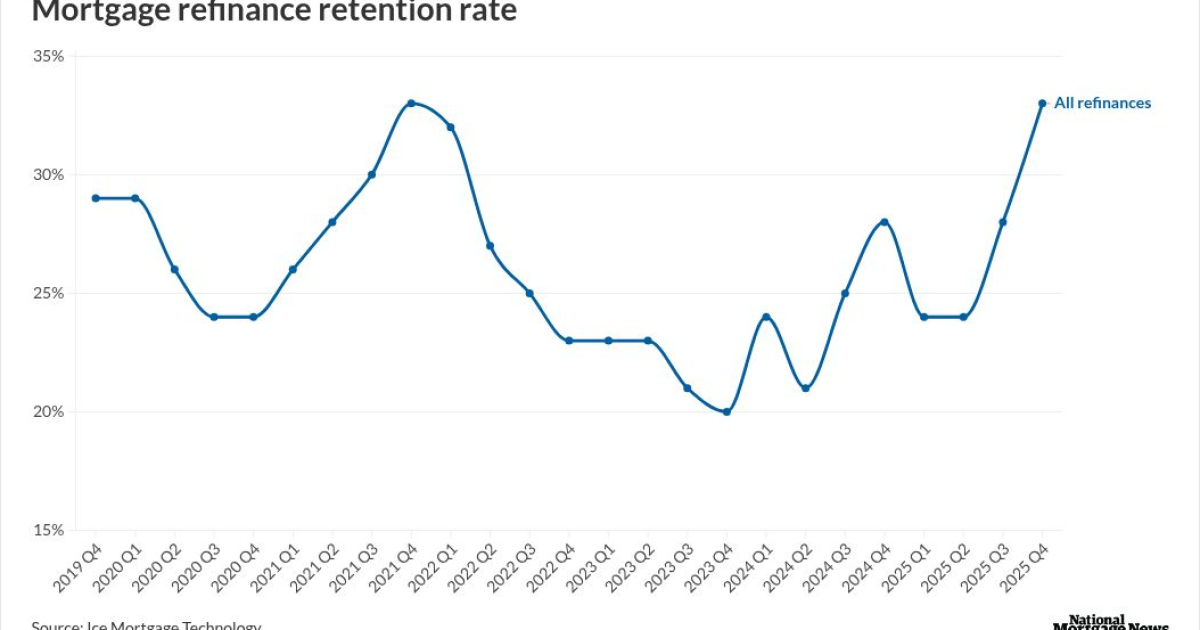

An estimated 565,000 first-lien refinances closed in the fourth quarter, up about 50% from a year prior and the most since the second quarter of 2022. This pushed total originations up to 1.44 million, according to ICE Mortgage Technology's latest mortgage monitor report.

"The fourth quarter marked a meaningful inflection point for mortgage market activity," said Andy Walden, head of mortgage and housing market research at ICE, in a press release Monday. "Refinances accounted for nearly 40% of Q4 lending and servicers retained one in three refinancing borrowers, the strongest overall retention rate since early 2014."

Retention among rate-and-term refinances also hit a 14-year high at 40%, with the average refinancer carrying a $510,000 balance and reducing their monthly payment by $248. Performance was especially strong for recently originated loans, as Federal Housing Administration and Department of Veteran Affairs loans led retention growth, the report found.

"Underpinning it all, February's dip in mortgage rates expanded the refinance-eligible population to 5.4 million borrowers, the largest pool we've seen since early 2022, further improving affordability, which is at its best level in

The 30-year fixed-rate mortgage interest rate

Home equity lending strong in Q4

Equity extraction also remained strong in the fourth quarter, as homeowners withdrew $52 billion in equity, bringing the 2025 full-year total to $205 billion, the most in three years. Of that amount, $116 billion was taken out through second liens, the largest annual second-lien volume since 2007, according to the report.

Homeowners hold nearly $17 trillion in total equity, with about $11 trillion considered tappable.

Home equity investment companies were active during the fourth quarter, as three

Property insurance costs hit an all-time high last year as well, rising 6.6%, which was the slowest pace since 2020. The fourth quarter also marked the first quarter-over-quarter decline in insurance costs since ICE began tracking monthly data in late 2023.

Taxes and insurance costs now make up an

"The trends we're observing underscore how quickly rate shifts can reshape borrower opportunity, lender volume and portfolio performance," said Bob Hart, President of ICE Mortgage Technology, in the release.