Rocket Mortgage and United Wholesale Mortgage waged another fight over who would be the market leader in 2025 and appear to have ended the year with a split decision.

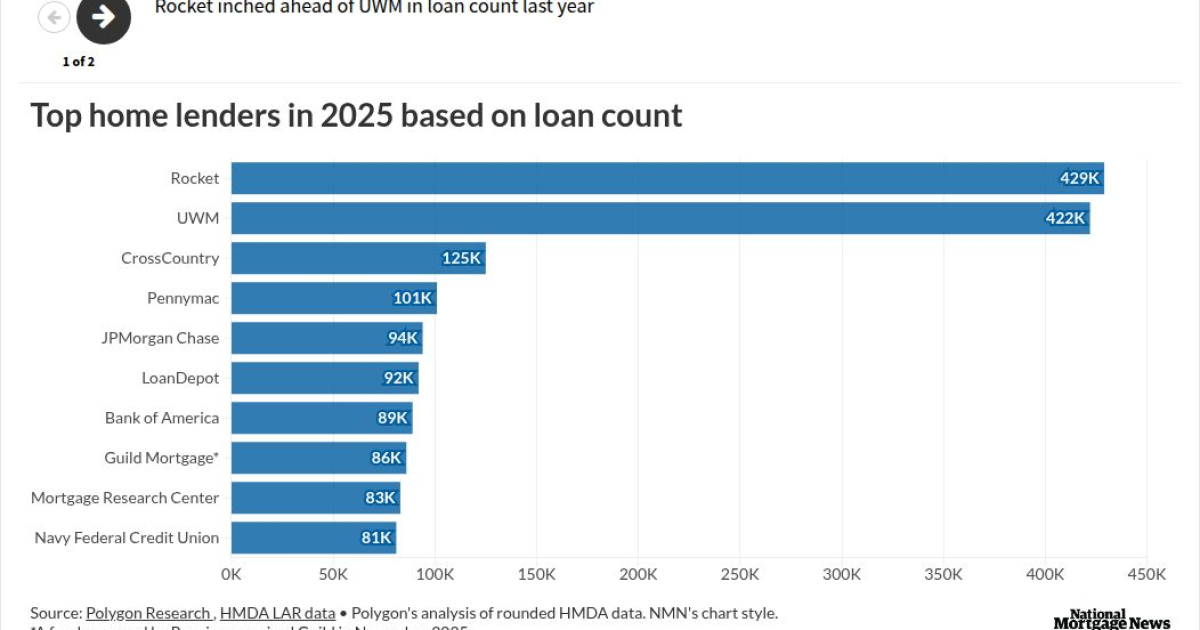

While UWM held onto a healthy lead in terms of dollar volume, Rocket inched ahead and became No. 1 based on loan count, according to Polygon Research's analysis of modified loan application register data from Home Mortgage Disclosure Act reports.

Rocket reported producing 429,332 loans in 2025 with a 6.33% market share, compared to 422,120 and 6.25%, respectively, at UWM. The wholesale lender had 366,078 loans and a 5.95% market share

"We see a different leaderboard by number of originations," Lyubomira "Val" Buresch, founder and CEO of Polygon Research, said in an interview about 2025's numbers.

What differentiated Rocket and UWM

"There are two distinct strategies for the top two lenders that are contending for the No. 1 position," Buresch added.

United Wholesale focused on homebuyer loans, while Rocket had higher volumes of cash-out refinances and

UWM easily surpassed Rocket based on dollar volume given its focus on purchase loans that typically have higher balances than cash-outs or seconds. Its loan volume was $164.32 billion and it had a 7.69% market share, compared with $116.16 billion and 5.44% at Rocket.

Rocket's data for last year might not reflect the full impact of its Mr. Cooper acquisition, which closed Oct. 1, 2025. There is often a lag between when a deal closes and two companies' numbers get combined for HMDA purposes, Buresch noted.

Mr. Cooper, which has reported into HMDA under its original Nationstar name, ranked 23 as an originator in 2025, according to Buresch.

Broader trends in HMDA data

The top 10 players controlled nearly one-quarter or more than 24% of the originations in 2025, according to Buresch.

Overall HMDA numbers do include some multifamily loans, which tend to have larger balances. So the loan count figure is generally a better indicator of the leaders in the single-family market.

Removing the multifamily component to focus on single-family does not change the composition of the top 10 much, other than to move No. 6-ranked nonbank LoanDepot up a notch to take JPMorgan Chase's position, Buresch said.

Several institution types report into HMDA, with the strongest loan count growth coming from nonbanks last year at 15%. Banks' loan counts were up 5%.

Primary mortgage growth ran at a rate around 10% last year, with subordinate liens up 9.2%.

Overall, last year's HMDA numbers show overall originations rose to 6.8 million from 6.25 million in 2024 with a decrease in the denial rate to 22.5% from 24.3%, according to a separate RiskExec HMDA analysis.

HMDA data available so far for 2025 contains more than 13.5 million records from more than 4,760 respondents. In 2024, there were 12.1 million records from around 4,900 respondents.