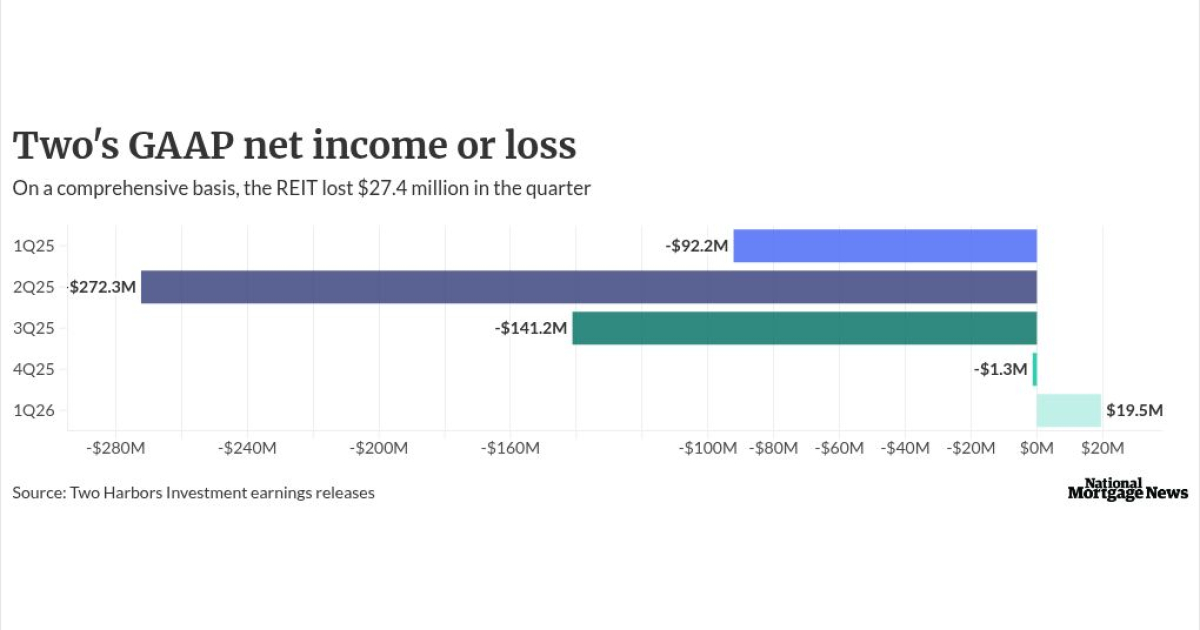

While Two Harbors Investment returned to profitability in the first quarter on a GAAP basis, the real estate investment trust reported a loss using a non-GAAP metric, comprehensive income.

Shares of Two Harbors rose 55 cents to $11.56 in the first 10 minutes of Wednesday trading, after CrossCountry raised its acquisition offer to $11.30 per share in cash following

During the earnings call, Bose George of Keefe, Bruyette & Woods asked if room exists for more unsolicited bids to come in until the May 19 special meeting for Two shareholders to vote on this transaction.

"The merger agreement's very prescribed, and lays out the details and the circumstances for how someone should do that if they were so interested," responded Bill Greenberg, president and CEO.

Two Harbor's first quarter financial results

In the first quarter, the real estate investment trust reported GAAP net income of $19.5 million, compared with

It is the company's first GAAP profit since the fourth quarter of 2024.

But it lost $24.7 million in the first quarter using a comprehensive income metric, which among other items includes net interest and servicing income, the mark-to-market calculations, operating expenses, taxes and preferred stock dividends.

At the start of the first quarter, Two Harbor's mortgage-backed securities performance was buoyed by the continued decline of implied volatility. This early positivity was enhanced by the Jan. 8 announcement by FHFA Director Bill Pulte at the direction of President Trump instructing

"However, mostly as a result of the

The quarter's impact on Two Harbors' book value

Two Harbors' book value was down 5% during the quarter, driven by the widening spreads in agency mortgage-backed securities, said Doug Harter, who now covers the company for BTIG, in a note put out before the earnings call.

"TWO's book value decline was broadly in line with Agency mREIT peers, which given the allocation to MSR is a modest disappointment," Harter wrote.

During the Q&A portion, Nick Letica, chief investment officer, pointed out that Two Harbors generally has a higher expense base than those peers because of the mortgage servicing business, RoundPoint. He also pointed out some of those others raised equity during the quarter.

"With those adjustments, I think that the portfolio performance would actually look relatively favorable," Letica said.

The drop in book value was below Keefe, Bruyette & Wood's estimates but in-line with what happened at other agency REITs, George said in his pre-earnings call analysis.

How RoundPoint did during the quarter

RoundPoint, Two's mortgage servicing business, has a small direct-to-consumer origination business, primarily to recapture those MSRs.

It funded $92 million in first and second mortgages, plus brokered another $38 million in second liens, Greenberg said. It also has $57 million in the pipeline.

"These are still small numbers, which to some extent are expected given the low note rate nature of our servicing portfolio," Greenberg said. "However, we believe the upcoming combination with CrossCountry should bring the origination efforts to a new level, and we expect that our recapture efforts should improve substantially, benefiting our servicing customers."

The bulk servicing transfer volume was $93 billion in the first quarter, compared with $154 billion in the fourth quarter, but just $60 billion one year prior.

"We continue to see most of the supply coming from non-bank originators with a broader array of buyer types, which include other non-bank originators, banks and REITs," Letica said.

RoundPoint has a $160.3 billion servicing portfolio as of March 31.

As for the housing market in general, Letica said inventory shortages are expected to keep putting upward pressure on prices, but "pockets of weakness" exist in some Southern markets, where

"Housing affordability, which had been improving since mid-2025,