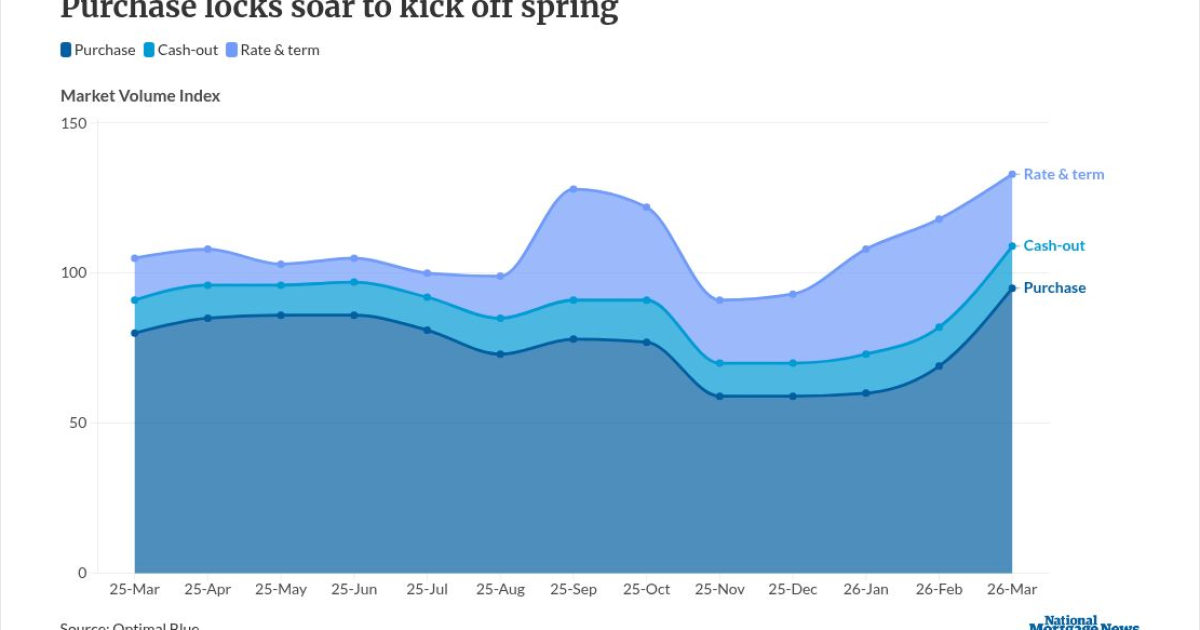

Purchase activity soared to kick off the spring market this year as climbing rates didn't dampen momentum over last year's tepid start.

Those mortgage locks in March were up 38% from February and 20% greater from the same time last year, according to

"That's a strong sign for the spring market, especially with refinance share still at 28%, well above where it spent most of 2025," said Mike Vough, senior vice president of corporate strategy at Optimal Blue, in a press release Tuesday.

Total rate lock volume rose 13% from February and 26% from last March, Optimal Blue reported.

Rate-and-term refinances meanwhile saw the biggest decline as monthly volume fell 34%, versus cash-out refi volume which ticked up 9% over the same period, according to Optimal Blue. Both products however remain well above last spring's levels, with rate-and-term and cash-out refis up 66% and 21% on an annual basis, respectively.

Pull-through across the industry has shifted. The pull-through rate for purchase loans of 80% in March was down 84 basis points from February, and down 569 basis points since the beginning of the year, Optimal Blue reported. The refi pull-through rate of 75.1% meanwhile rose 157 basis points last month and has grown 588 basis points in the past three months.

Inside the numbers

The average loan amount inched down to $401,000 from $404,586 in February, while the average loan-to-value ratio was 81.32%, according to the report. Debt-to-income ratios meanwhile remained under year-ago levels, with the purchase DTI at 36.3% for conforming loans, and the DTI for Federal Housing Administration-backed loans at 43.3%.

In the

In March, mortgage servicing rights for conforming 30-year loans ticked up 6 basis points to 1.24%, representing a 4.97 multiple, Optimal Blue found. Lenders are also cashing out quicker, as hedged loan sales to the agency cash window rose 100 basis points last month to 28%.

"We saw some movement toward the cash window in March, but the more telling signal was MSRs moving higher as refinance expectations came down," said Vough. "That's the market adjusting to a higher-rate backdrop."