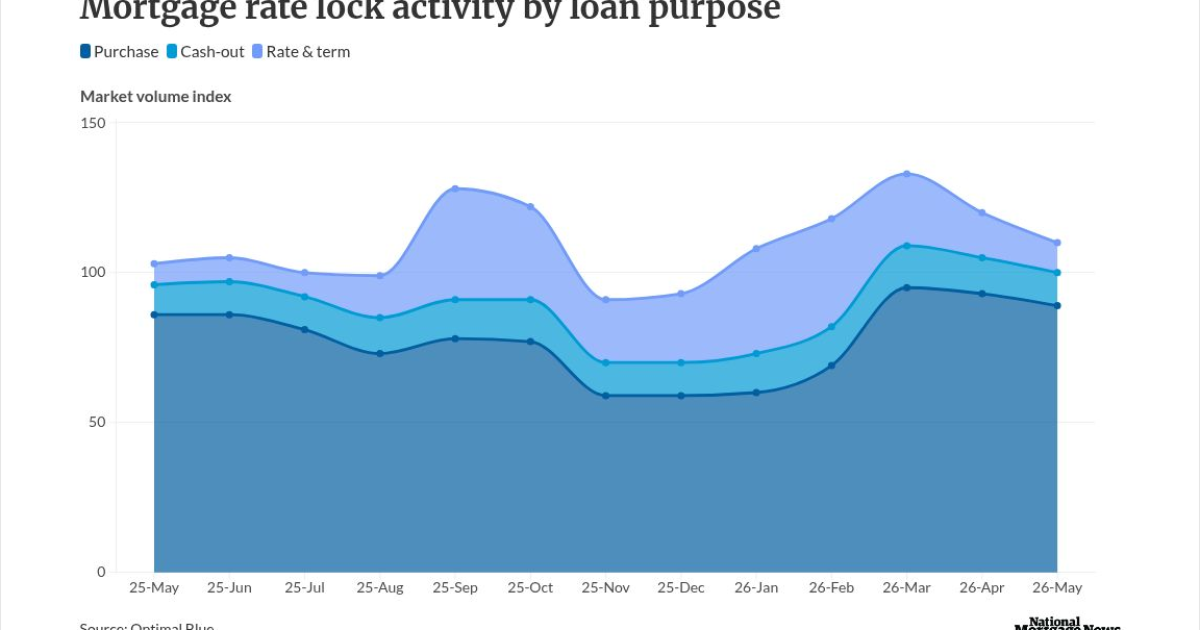

Rising mortgage rates led loan volume to shrink in May, while declining pull-throughs suggest some borrowers are changing plans in the midst of current volatility, according to the latest Market Advantage report from Optimal Blue.

The product-pricing engine and secondary trading platform reported mortgage lock volume down 5.4% on a monthly basis in May, with the

Compared to last year, lock activity still managed to finish ahead of May 2025's pace by 6.7% overall. Purchases increased 3.5%, with cash-out refis up 7.2% and rate-and-terms higher by 46.1%.

The changes in lock activity came during a month where the 30-year conforming fixed rate increased 13 basis points to 6.44%, according to Optimal Blue data. A mortgage development to keep an eye on may be occurring after borrowers lock, said Mike Vough, senior vice president of corporate strategy

"Pull-through rates declined across both purchase and refinance pipelines, which tells us borrowers are closely monitoring changes in the rate market," he added.

Purchase pull-throughs came in at 76.7%, a month-to-month decrease of 539 basis points. The same rate for refinances dropped 1,332 bps to 65.3%. On a year-to-year basis, purchase pull-through activity fell back by 636 basis points, but refinances remained 304 bps above its May 2025 mark.

The secondary market also showed changing seller preferences last month, "reflecting the impact of agency execution strategies and/or specified pay-up impacts," Vough said.

Executions of agency mortgage-backed securities retreated to 41% from 44% in April. At the same time, cash executions grew to a 32% share from 28%.

Even with a large proportion of overall originations, purchase activity retreated 3.5% month over month. Refi volumes took an even steeper dive compared to purchases amid ongoing rate pressure, with cash-out transactions down 12.8% from April and rate-and-terms falling 33.6%.

"Purchase activity continues to be the loan-purpose leader in spite of affordability pressures," said Vough. "More than four out of five mortgage locks were tied to purchase transactions in May."

Purchases accounted for an 81% share of all locks, with refinances taking the remaining 19%, which was the smallest slice since June 2025.

Loan-type mix shifts

Meanwhile, in a sign of shifting borrower preferences, the conforming share of mortgage locks made up less than half of volume for a second straight month, accounting for 48.9% of activity. Locks for

Non-conforming mortgages represented 18.7% of May lock volume. Within the segment, non-qualified activity increased to a 9% share of the total market.

Seeing a recent resurgence, adjustable-rate mortgages expanded to 11% of production last month, the second-highest percentage since October 2022.

The average loan amount within May's locked volume grew 0.4% to $395,535, compared to $394,046 the previous month. Average loan-to-value ratio was 81.6%, Optimal Blue's report said.