Reduced projections for interest rate cuts this year has lenders mulling the extent to which they need to diversify their product sets, several experts at an industry conference said Wednesday.

"Inflation is starting to move through the system and I think it's going to keep rates elevated for quite some time," Scott Buchta, managing director and head of fixed income strategy at Brean Capital, said at the IMN/Informa Residential Mortgage Securitization meeting in New York.

Buchta said he anticipated largely stable rates through the year with possibly one cut in short term financing costs that federal policymakers control.

Policymakers have

That suggests that while small mortgage rate drops — like

As a result, lenders may have to focus more on what Al Qureshi, CEO and cofounder of Black Lake Investments, called "the other refi boom," referring to nontraditional products like second liens that borrowers may still have reasons to be interested in regardless of rate incentive.

"I see a lot of that activity continuing," he said.

Older households with homes more likely to need renovation have created some persistent demand for home equity products, noted Roger Ashworth, head of research and data at Saluda Grande.

While younger consumers are struggling to afford their first home, limiting purchase mortgages and stretching the finances of those who get them, older borrowers with houses need to maintain them and might have some disposable income but still need help paying for repairs.

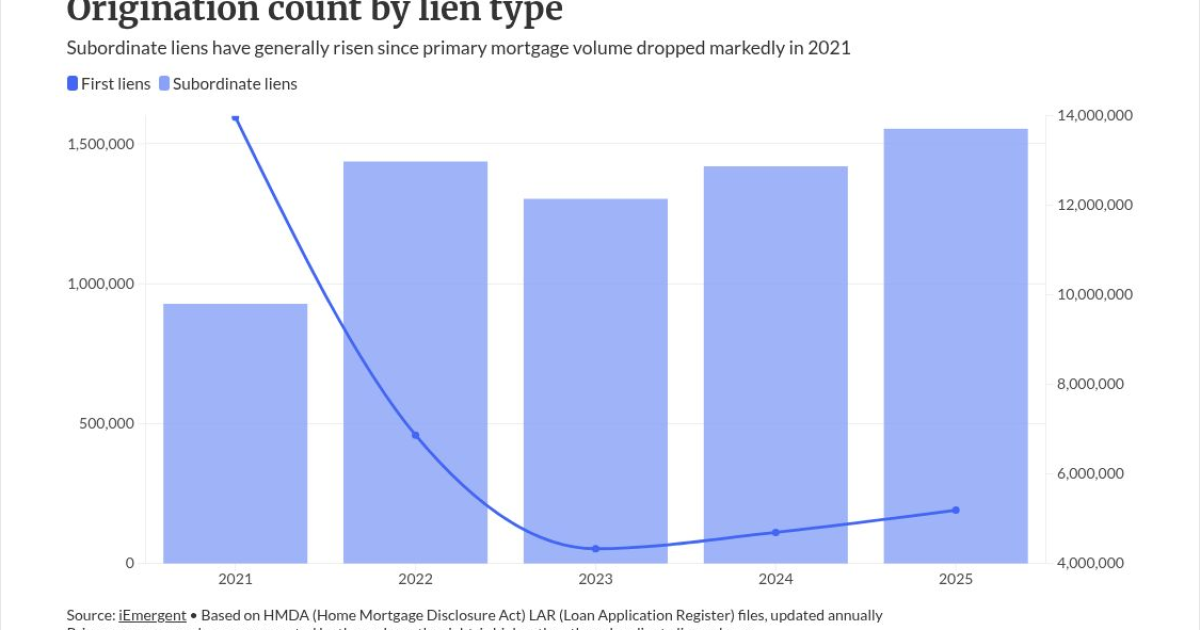

The housing finance industry's reliance on subordinate liens is evident from

Where the challenges lie

However, another cut of HMDA data points to some of

Based on dollar balance, subordinate liens only represented a little over 8% or $175.39 billion of the $2.12 trillion in total home lending recorded in HMDA data.

Also, nonbank mortgage players that have increasingly become involved in

Homeowners' ability to repay also could come under more stress in some areas. Tax assessments lag home price movements, so while housing valuations may be stabilizing or falling in some areas, homeowners may be overpaying during a transitional period.

"We see it in our servicing portfolios," Qureshi said, noting that the amount involved can be "material."

This trend may add negative advancing responsibility for servicers but could have an upside for some depository institutions.

"If you're a bank, you like higher escrow float income," he said.