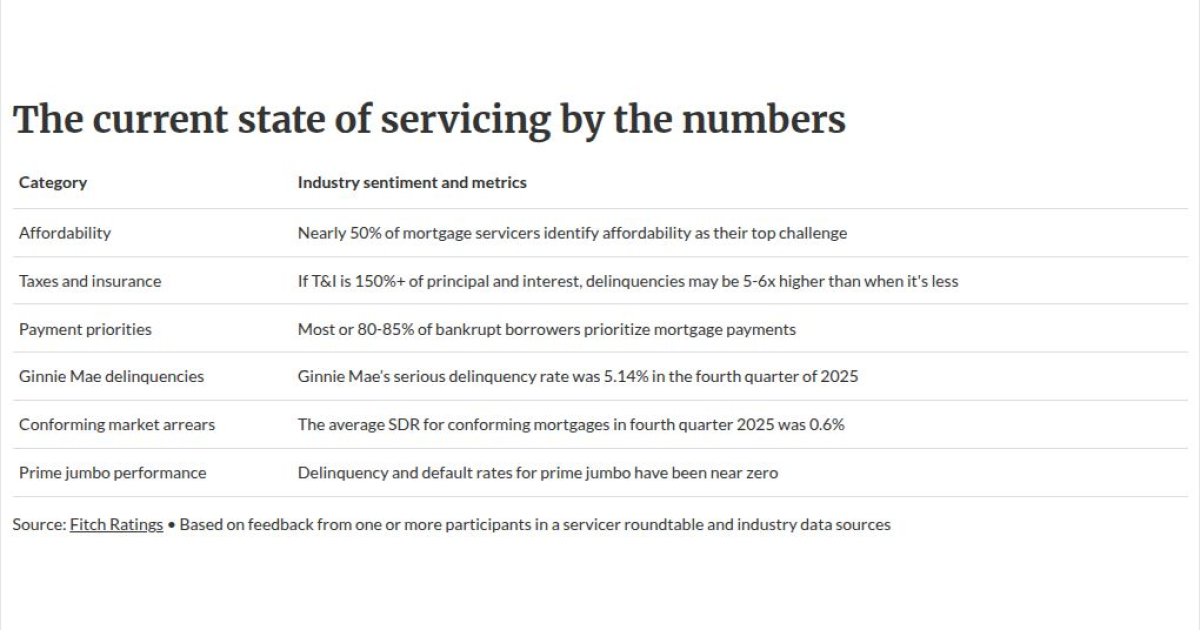

Almost half of servicers have mixed views on whether affordability is their main challenge, according to a new Fitch Ratings report.

Nearly half of mortgage servicers at a recent roundtable the rating agency held identified it as such, in line with ongoing debate over how much of stress there is on loan performance from

Broader feedback reported from servicers, taken together with recent industry data they've been looking at, suggesting that the key concerns they've been wrestling with come from product-specific developments in addition to affordability strains.

Performance and products

Where affordability is a concern, one servicer told Fitch they've found the size of

In cases where the T&I payment is 150% or more of the principal and interest obligation, delinquencies may be 5-6 times higher than when it's less, according to Fitch.

Servicers told Fitch to date most or 80-85% of borrowers declaring bankruptcy have been prioritizing their mortgage payments over other forms of debt.

In line with other reports, Fitch's shows mortgages made to lower-income borrowers whose loans are in Ginnie Mae guaranteed securitizations had a markedly higher serious-delinquency rate of 5.14% in the fourth quarter of last year, vs. 0.6% for the conforming market and near-zero defaults and arrears for prime jumbo.

While that may suggest in part that affordability pressures are concentrated there, some experts recently reacting to Fitch's report reaffirmed Ginnie's view that recent Federal Housing Administration rule changes have been a more influential driver of the elevated SDR rate.

"FHA loans in trial payment plans used to be counted as cured when the plan started, and now they are only counted as cured once the trial is completed. That change alone can make serious delinquency look worse," said Mirza Hodzic, managing director of Black Wolf, in an email.

Operational issues

Procedural changes that have led to dramatic shifts in operational responsibilities have also been part of the challenge, according Donna Schmidt, president and CEO, DLS Servicing.

"The collection department, single point of contact (SPOC) staff, has had to make a hard turn from coaxing borrowers to simply apply for loss mitigation to educating borrowers their choices," she said in an emailed statement.

Other operational challenges servicers have been facing stems from a wave of acquisitions taking place and specialty product needs outside the standard qualified-mortgage definition.

"Challenges were noted in servicing specialty loans such as various types of business purpose loans, which are driving much of the

The vast majority or 75% of servicers identified automating operations for these loans as the primary concern in this market.

Servicers are selectively applying artificial intelligence to repetitive tasks that include payment processing and tax document requests, reducing these types of call center responsibilities, but they stressed the need for human oversight of the workflows amid state regulatory oversight.

Fitch's insights stemmed from feedback received from 27 representatives of 20 companies, including master servicers, during a roundtable focused on the domestic residential mortgage-backed securities market.