With interest

However, following recent Federal Reserve policymakers' signals that rate cuts loom this year, analysts also anticipate bankers' commentary during earnings calls will include

The Fed has not raised rates since last summer. But after pushing up its benchmark several times in 2022 and early last year, it holds near the high point of this century, keeping deposit costs elevated for banks and interest expenses high for borrowers. This has curbed loan demand and squeezed the margin between what banks earn on lending and pay out on deposits.

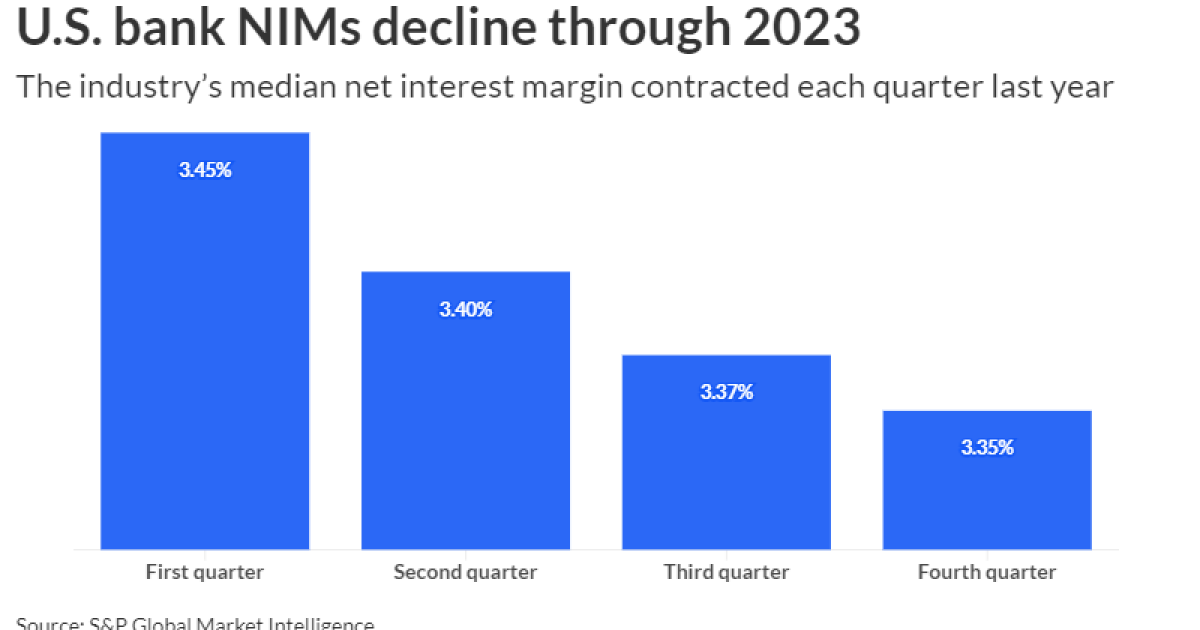

U.S. banks' median net interest margin, a key measure of profitability, declined to 3.35% in the fourth quarter, down 2 basis points sequentially after slipping 3 basis points in the third quarter and 5 basis points in the second quarter of last year, according to data from S&P Global Market Intelligence.

First-quarter results are expected to show that downward NIM pressure persisted through the early months of this year. High rates also have hampered more consumers and commercial real estate borrowers. Credit card costs spiked alongside rates, making monthly payments higher and more difficult to manage, and CRE office properties, in particular, have struggled because of enduring remote work trends in the aftermath of the pandemic.

The annualized fourth-quarter net charge-off rate in the credit card segment rose 94 basis points from a year earlier to 4.15%, the highest level since this metric reached 4.38% in the second quarter of 2019, according to S&P Global. Total delinquent CRE loans stood at $25.26 billion at the close of 2023, up 79% from a year earlier.

Wedbush analyst David Chiaverini said high rates "may continue to pressure negative credit migration, especially for banks with outsized exposure to CRE and consumer loans."

These headwinds, in turn, are slowing down the economy.

Yet, as Iron Bay Capital President Rober Bolton said, the industry overall remained profitable throughout 2023 and is expected to remain so this year. Profits also are poised to increase in the second half of 2024 and into next year should the Fed follow through on the three rate cuts that policymakers said were likely in a report after their March meeting.

"So it's still hard to predict when exactly the Fed will start to move, and there's still plenty of uncertainty around a slowing economy and what that means for the near term," Bolton said. "But longer term, assuming the Fed does act, margins will benefit, and I think there's good reason to be optimistic about community banks."

That view is in sync with the American Bankers Association's

The committee sees economic growth around 1.7% for 2024 and 1.8% for 2025. The forecast for this year would accelerate an already slumping pace. Gross domestic product advanced at an annual rate of 3.2% in the fourth quarter, down from third-quarter growth of 4.9%, according to the U.S. Department of Commerce.

Employers collectively reported six-figure job gains every month last year — and again in January and February of this year but the rate has eased. Employers added

Employers added 225,000 jobs per month, on average, in 2023. The ABA economists see that slowing to 139,000 per month in 2024 and declining to just about 117,000 in 2025. The committee sees the unemployment rate reaching 4.1% by the end of 2024, up from 3.9% in February and 3.7% at the end of last year.

"The cumulative effect of still-high interest rates, softening demand, lower consumer savings and a mild uptick in unemployment will drive some deterioration in credit quality," said Simona Mocuta, ABA committee chair and chief economist at State Street Global Advisors.

The ABA forecast anticipates bank consumer delinquency rates will increase slightly from 2.8% in 2024 to 2.9% in 2025. That would be up from an estimated 2.4% last year.

But recession risks have diminished, the ABA committee said, and inflation continues to be moderate, opening the door for rate cuts beginning this summer. At a

The consensus view of the committee is that the Fed will begin cutting the target federal funds rate range in mid-2024, instituting three 25 basis point cuts before the end of this year. The reductions would help lower deposit costs and potentially drive stronger loan demand. With more loan volume, and lower costs to fund loan growth, banks could drive stronger net interest income and, by extension, profitability.

Against that backdrop, Piper Sandler analyst Casey Orr Whitman said that, across his firm's coverage universe, loan growth slowed and funding costs rose throughout 2023, and likely did so during the first quarter. This hindered margins and, by extension, earnings per share.

For the first quarter, Whitman estimated a sequential NIM decline of 3 basis points and a 7% linked-quarter decrease in core EPS for the industry

"The sustained higher interest rate environment and continued economic uncertainty help drive near-term and intermediate-term softness," Whitman said.