Home Equity Conversion Mortgages endorsements fell for the second month in a row in April, although trends show proprietary reverse products are now filling some of the void.

Endorsements of the Federal Housing Administration-backed product dropped 1.4%

The April number also pulled back from 2,320 endorsements in the same month one year ago.

At the same time that HECM demand appears to be waning, proprietary reverse liens are picking up, demonstrating consumer interest in equity-draw products is not necessarily on the decline.

"The regional growth/decline picture looks a lot like you'd expect if HECM volume was being undercut by proprietary reverse mortgage market share," RMI said.

"In looking at eight currently available proprietary RM products, there is a distinct relationship between HECM growth rates and proprietary product availability," the data intelligence provider continued, without naming providers.

Reverse lenders, including the

Recent first-quarter data also underscores the shifting trend, with New View Advisors reporting the proprietary share of reverse originations between January and March grew to 52% of the market. Volumes of proprietary production surged to approximately $953 million during the first quarter, surpassing the HECM total of $875 million, New View Advisors said.

April HECM data

Between March and April,

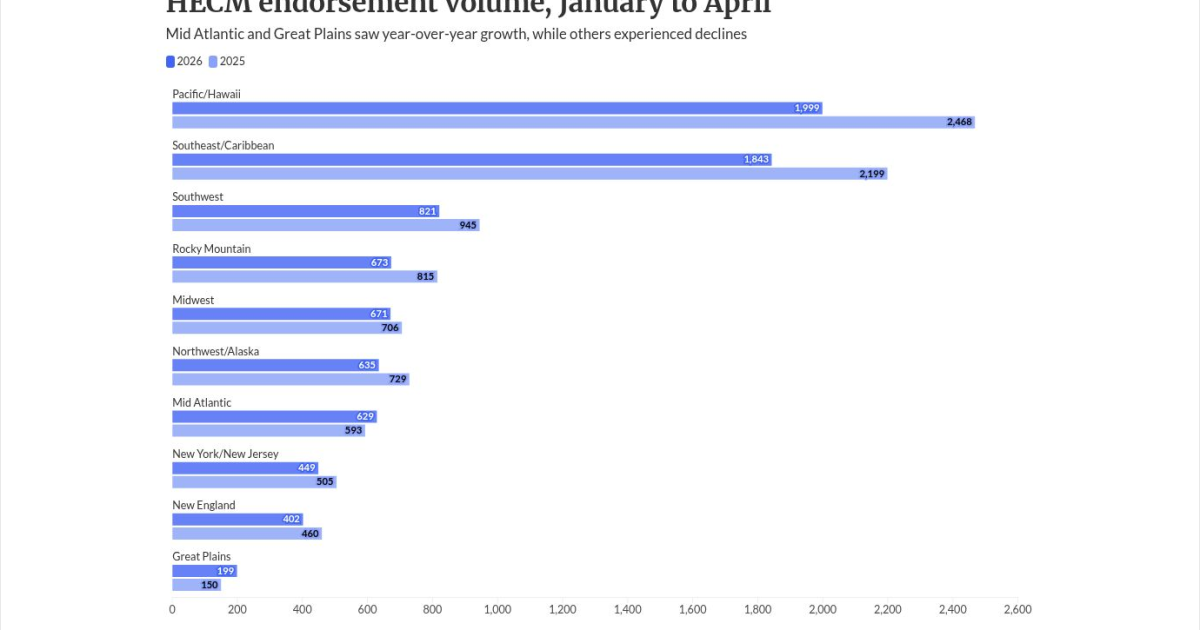

Of note, though, is the year-to-date trend, which shows only two regions in the country experiencing 2026 HECM growth: Great Plains and Mid Atlantic. Both happen to contain states with minimal proprietary reverse mortgage availability, RMI said.

The two regions also reported month-to-month increases in April alongside the Pacific/Hawaii and Rocky Mountain regions.

Among individual lenders, Mutual of Omaha Mortgage took back the No. 1 position from Finance of America with 497 endorsements compared to the latter's 394. Longbridge Financial landed in the third spot with 367, followed by Goodlife Home Loans at 125 endorsements.