Even if he was so-inclined to do so, President Trump might not be able to unilaterally release the government-sponsored enterprises from conservatorship because of the U.S. Supreme Court tariff ruling, a BTIG analyst report postulates.

Since Feb. 13, with the exception of Feb.18, mortgage rates have been under 6%, reaching 5.9% on Feb. 27, the Optimal Blue website said. This is the last date Optimal Blue publicizes data for.

But the attack on Iran has driven the 10-year Treasury higher by 9 basis points ending March 2 trading at 4.05%.

"On Friday, we saw US Treasury yields drop to multi-month lows on the prospects of the Iran situation breaking out," Louis Navellier, an investment banker, said in a commentary on Monday. "Today, it's moving back the other way on the inflation threat of the much higher energy prices."

What happened with mortgage rates and GSE stock prices

Lender Price data listed on the National Mortgage News website on Monday morning had the 30-year FRM at the 6.04% mark at 11 a.m. Three hours later, it was up to 6.12%.

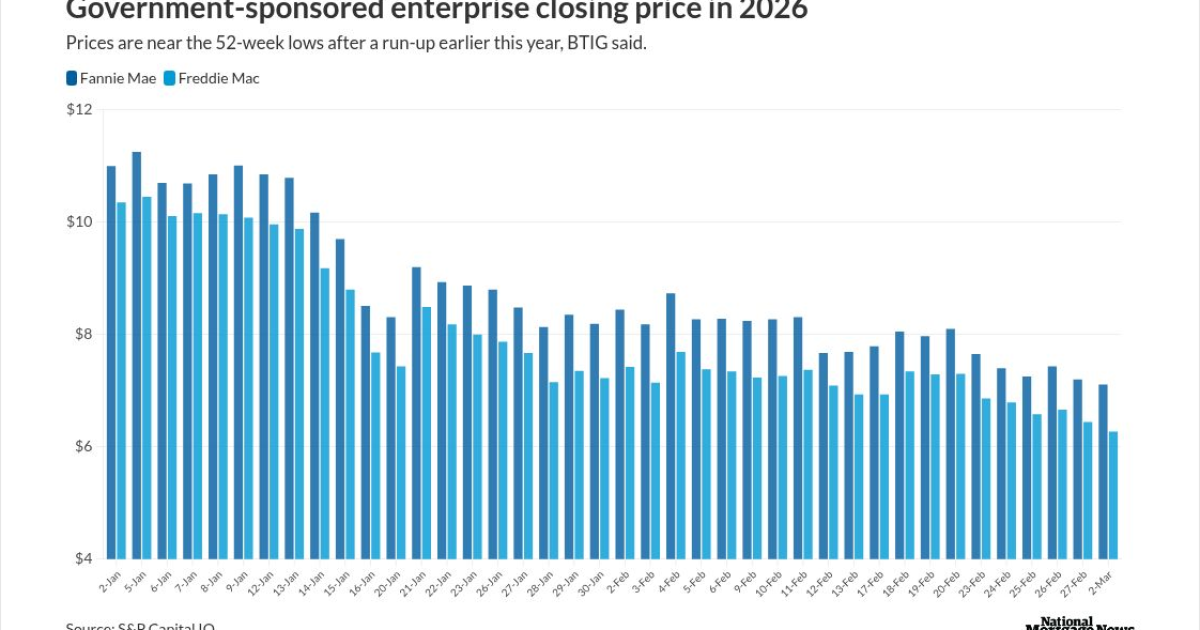

Freddie Mac closed on March 2 at $6.27, similar with levels seen nearly a year ago. Meanwhile Fannie Mae was at $7.11 per share, a point last seen in May 2025. Hagen's report came out before the market opened Monday morning.

"Stock valuations for the GSEs have almost fully retraced to their 52-week low seen just shortly after Trump assumed office, and the stocks are down 40% since the MBS directive was announced," Hagen said. "Speculation surrounding recap and release steadily gained momentum last year after Trump onboarded Bessent and Pulte, which culminated in a 52-week high of $14/share in September."

Accounts on X have been consistently imploring the Administration to at least follow Bill Ackman's suggestion

Can the GSEs be released soon

Hagen says the consensus (without identifying where the consensus comes from) is a near-term release is "more remote, we think mainly on the belief that Trump could desire even more control around mortgage rates, which could weaken the earnings trajectory and attractiveness of the stocks in a relisting scenario.

"Plus, we think the

The 6-3 ruling by the Supreme Court said the president cannot act unilaterally under the International Emergency Economic Powers Act. Whether this could apply to other actions is an open question.

At

"So before anybody could consider maybe doing something and raising money from the public, aren't there some other decisions that we have to take into account?" Hill asked industry panelists at the hearing. "Like, wouldn't the Treasury Department have to make a concrete decision about how much money they're still owed from the financial crisis or not owed?"

Has the effect from the MBS purchase directive worn off?

The

Fannie Mae added $8.5 billion of agency MBS and Freddie Mac, $4 billion, to their respective retained portfolios following Pres. Trump's Jan. 8 directive, Hagen noted. Data shows both companies'

The impact of those purchases first affects lenders in the mortgage-to-Treasury/SOFR spread, said Mike Vough, Optimal Blue's senior vice president of corporate strategy.

"As current coupon spreads compress, we typically see it translate into sharper borrower pricing and more predictable hedge performance, even if it's not a perfect one-for-one move." Vough said, noting those contracted by 12.5 basis points immediately after the President made his announcement.

"As broader macroeconomic factors took center stage, however, spreads widened 7.5 to 10 basis points, suggesting the impact was more fleeting alongside Treasury movement," Vough said. "Even so, spreads remain well above the ultra-wide levels of 2024, so disciplined execution and risk management still matter. In a market where policy can influence spreads, lenders need pricing, hedging and analytics working in lockstep."

Another benefit of the spreads initially tightening was that it

"For depositories, it's not a shunned asset anymore," he said, especially as the market moves further away from the 2021-2022 lending environment. The reasons are independent from recent talk by Federal Reserve Vice Chair for Supervision Michelle Bowman about changes to the Basel III framework.

"They had a duration and a concentration risk issue with the asset for a while," Toohig said. "Now that we have more current coupons and they're able to originate loans at much higher yields, it's an asset that they're more comfortable with."

The gain in adjustable rate mortgage market share, another product primarily done by depositories, also has contributed, he continued.

What might move a release of the GSEs is the upcoming mid-term elections. Those typically go against the party in power, and as long as the ducks are in a row with the White House and Congress in Republican control, ending the conservatorships are a possibility.

After both Fannie Mae and Freddie Mac reported

"Given our view that either the status quo of conservatorship will persist or a meaningful dilution of the common shares is likely to occur if GSE privatization does get over the finish line, we remain underperform on both Fannie Mae and Freddie Mac," George said.